China’s Drone and Commercial Space Race: How Private Companies Are Competing with State Programs

In the skies above Chinese farmland and in the orbital paths circling Earth, a remarkable transformation is unfolding. China’s drone and commercial space race has evolved from a state-dominated industry into a dynamic battleground where nimble private companies are challenging—and sometimes surpassing—government-backed programs. While DJI commands over 70% of the global consumer drone market, a new generation of Chinese innovators is pushing boundaries in agricultural automation, delivery logistics, and even reusable rocket technology. This surge in private sector innovation represents more than just technological advancement; it signals a fundamental shift in how China approaches emerging industries and global competitiveness.

China’s Drone and Commercial Space Race: How Private Companies Are Competing with State Programs has accelerated dramatically in 2026, with private enterprises leveraging cost advantages, agile development cycles, and specialized expertise to carve out lucrative niches both domestically and internationally. From Unitree Robotics’ advanced automation systems to LandSpace’s Zhuque-3 reusable rocket program, Chinese private companies are demonstrating that innovation can flourish alongside—and sometimes ahead of—state-sponsored initiatives.

Key Takeaways

- 🚁 China operates over 300,000 agricultural drones—more than 60% of the world’s total—establishing dominance in unmanned farming technology[3]

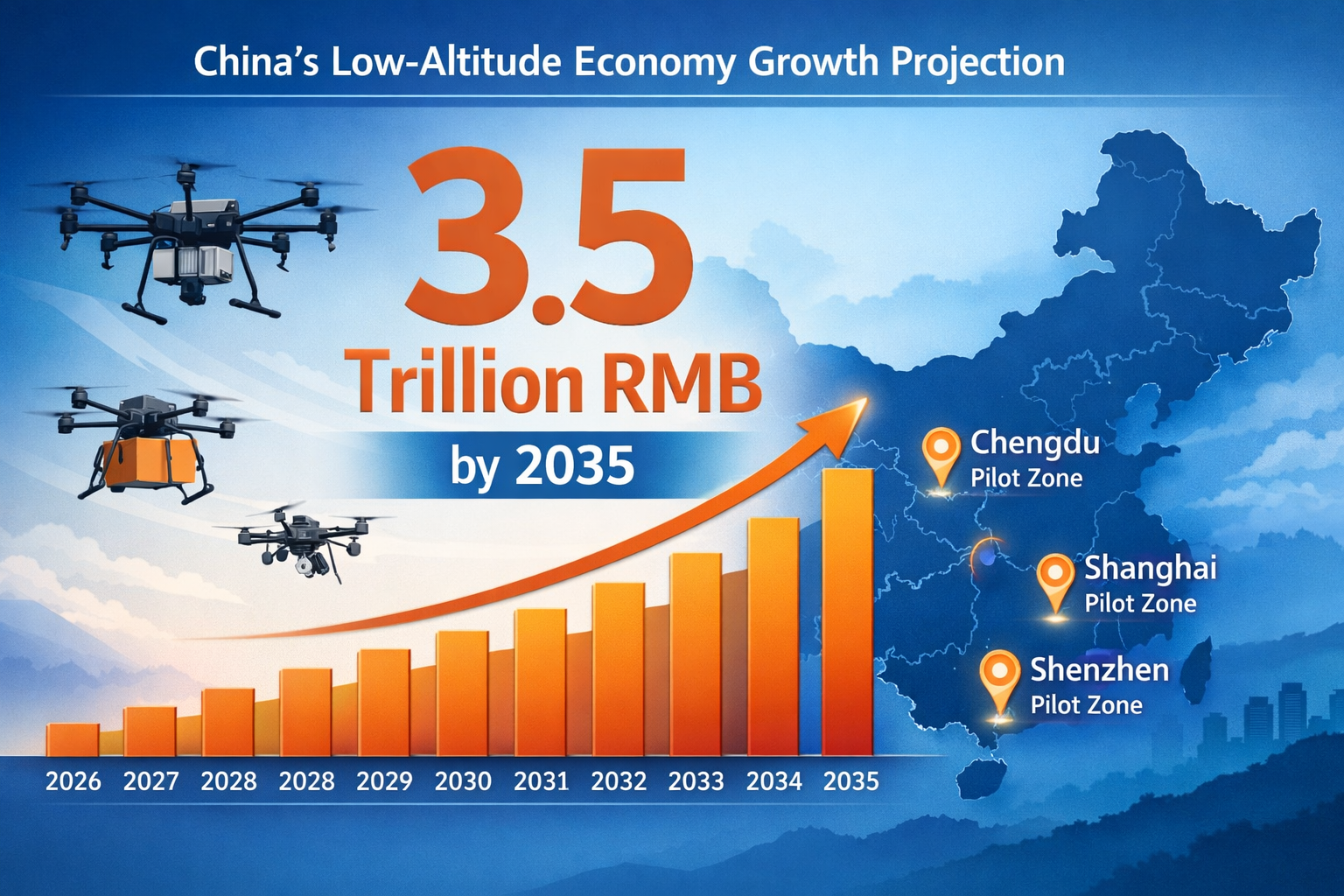

- 💰 The low-altitude economy could reach RMB 3.5 trillion ($502 billion) by 2035, driving massive investment in commercial drone infrastructure[1]

- 🌍 Domestic market saturation is forcing Chinese drone makers to expand internationally, with companies like Aerospace Times Feipeng targeting Southeast Asia and the Middle East[2]

- 🎯 Private companies maintain significant cost advantages through vertically integrated supply chains, with inspection drones priced between $40,000-$200,000—far below Western competitors[2]

- ✈️ New regulations taking effect in July 2026 will formalize the industry while raising barriers to entry, potentially consolidating market power among established players[1]

The Rise of China’s Low-Altitude Economy

China’s commitment to developing what officials call the “low-altitude economy”—commercial airspace below 1,000-4,000 meters—represents one of the most ambitious infrastructure projects of the decade. The Civil Aviation Administration of China (CAAC) projects this sector could exceed RMB 3.5 trillion (US$502.23 billion) by 2035, transforming how goods move, crops are managed, and emergency services respond[1].

Pilot Zones Leading the Transformation

Four major cities are pioneering this aerial revolution:

| City | Specialization | Notable Achievement |

|---|---|---|

| Shenzhen | Drone cargo logistics | Hundreds of commercial delivery routes operational |

| Shanghai | Urban air mobility | eVTOL passenger trials underway |

| Chengdu | Industrial inspection | Automated infrastructure monitoring networks |

| Shijiazhuang | Emergency services | Rapid medical supply delivery systems |

These pilot zones serve as testing grounds where private companies and state programs collaborate and compete to establish operational standards, safety protocols, and viable business models. Shenzhen alone has established hundreds of drone cargo routes, demonstrating the commercial viability of automated aerial logistics[1].

The regulatory framework supporting this expansion is becoming more sophisticated. Revised aviation rules taking effect in July 2026 will require all drone design, manufacturing, and operations to obtain CAAC certification and mandatory electronic identification[1]. While these requirements improve safety and traceability, they also raise market entry barriers—a development that favors established private players with resources to navigate complex compliance requirements.

Agricultural Dominance: Where Private Innovation Meets State Support

China’s agricultural sector showcases how private companies are competing with state programs while simultaneously benefiting from government policy support. The country operates over 300,000 agricultural drones—more than 60% of the roughly 500,000 in service globally—establishing China as the undisputed leader in unmanned farming technology[3].

Policy Elevation Signals Long-Term Commitment

The significance of this sector received unprecedented recognition when China’s government released its No. 1 Central Document on February 3, 2026. For the first time in the history of this annual policy blueprint, drones and robots were placed at the center of agricultural priorities[3]. The document designates unmanned systems as “indispensable tools” for farmers, signaling sustained government commitment to the sector.

This policy support creates a favorable environment for private drone manufacturers like XAG, which specializes in agricultural automation. The company has expanded its product line from traditional crop protection and seeding applications to sophisticated farmland monitoring and agricultural logistics systems[3]. By combining artificial intelligence with precision agriculture, these private companies are delivering solutions that state research institutions alone could not develop at comparable speed or scale.

Key applications driving agricultural drone adoption:

- 🌾 Precision crop spraying – Reducing pesticide use by 30-40% through targeted application

- 🌱 Automated seeding – Covering terrain inaccessible to traditional machinery

- 📊 Real-time field monitoring – Using multispectral imaging to detect crop stress

- 📦 Agricultural logistics – Transporting supplies to remote farming operations

DJI’s Global Dominance and the Competitive Landscape

No discussion of China’s drone industry would be complete without examining DJI’s remarkable market position. The Shenzhen-based company commands over 70% of the global consumer drone market, with its products used by everyone from hobbyist photographers to Hollywood film studios. However, DJI’s dominance has created both opportunities and challenges for China’s drone ecosystem.

Beyond DJI: The Emerging Competitors

While DJI captures headlines, multiple high-performing private companies are carving out specialized niches in China’s drone and commercial space race:

JOUAV focuses on industrial-grade fixed-wing drones for surveying and mapping, competing directly with Western manufacturers like senseFly and Wingtra. Their systems offer comparable performance at significantly lower price points, making them attractive to international customers in developing markets.

Autel Robotics targets the prosumer and enterprise segments with foldable drones that compete directly with DJI’s Mavic and Phantom series. The company has invested heavily in avoiding DJI’s intellectual property, creating truly differentiated products rather than mere clones.

XAG dominates agricultural automation with fully autonomous crop-spraying systems that integrate with precision farming software. Their platform approach—combining hardware, software, and agronomic data—creates higher switching costs and customer loyalty than simple drone sales.

EHang stands out as the only publicly traded eVTOL (electric vertical takeoff and landing) company to receive domestic approval and begin actual passenger-carrying operations, though currently limited to China[4]. Their autonomous air taxi trials represent the cutting edge of urban air mobility.

According to industry research, Chinese drone companies prioritize Marketing & Sales, software development, and hardware leadership as their core competitive advantages[4]. However, optimism levels among Chinese firms rank slightly below the global average (6.2 vs. 6.6), partly due to protectionist measures in major markets like the USA and India that restrict Chinese drone imports[4].

Domestic Market Saturation Drives International Expansion

The very success of China’s drone industry has created an unexpected challenge: intense domestic competition that squeezes profit margins and limits growth opportunities. Chinese drone manufacturers now face a stark choice—fight for shrinking margins at home or pursue international expansion despite geopolitical headwinds.

Aerospace Times Feipeng’s Global Pivot

Aerospace Times Feipeng exemplifies this strategic shift. At the Singapore Airshow in early February 2026, the civilian drone maker unveiled two new inspection models designed specifically for international markets[2]:

- Premium inspection platform – Priced between $180,000-$200,000, targeting infrastructure monitoring and industrial applications

- Specialized emergency response drone – Priced between $40,000-$50,000, optimized for forest fire detection and maritime rescue operations

The company reported annual revenues exceeding 100 million yuan ($14.4 million) for two consecutive years, demonstrating commercial viability despite domestic market pressures[2]. Feipeng’s competitive advantage stems from its fully domestic supply chain, which enables cost structures that Western competitors cannot match without sacrificing performance.

The company’s international expansion targets Southeast Asia and the Middle East—regions with growing infrastructure investment, less stringent technology restrictions, and price sensitivity that favors Chinese manufacturers[2]. This geographic diversification strategy is becoming standard among Chinese drone companies seeking to escape domestic market saturation.

The Cost Advantage Challenge

Chinese manufacturers maintain structural cost advantages through vertically integrated domestic supply chains. Components that Western drone makers source from multiple international suppliers can be procured domestically in China, often from the same industrial clusters that produce components for consumer electronics.

This integration allows Chinese companies to:

- ⚡ Reduce development cycles from concept to production

- 💵 Undercut Western pricing by 40-60% on comparable systems

- 🔧 Iterate rapidly based on customer feedback

- 🌐 Scale production quickly to meet demand spikes

However, these advantages come with limitations. Geopolitical sensitivities around Chinese technology remain key risks to global expansion ambitions, alongside regulatory hurdles in Western markets that increasingly view Chinese drones as potential security threats[2]. The AI tools and autonomous capabilities that make Chinese drones competitive also raise concerns about data security and surveillance applications.

Military Applications: State Programs and Private Partnerships

While commercial drones capture consumer attention, China’s military drone programs represent a significant dimension of the country’s drone and commercial space race. Here, the relationship between state programs and private companies becomes more complex, with private manufacturers often serving as suppliers and partners to state-owned defense enterprises.

Combat Drone Export Success

The state aerospace manufacturer Aviation Industry Corporation of China (AVIC) displayed the WL-X maritime combat drone—the latest member of the Wing Loong family—for the first time in Southeast Asia in February 2026[5]. This unveiling at the Singapore Airshow signals China’s growing confidence in exporting advanced military systems.

Existing Wing Loong operators include:

- 🇸🇦 Saudi Arabia

- 🇦🇪 United Arab Emirates

- 🇪🇬 Egypt

- 🇵🇰 Pakistan

- 🇲🇦 Morocco

- 🇩🇿 Algeria

- 🇮🇩 Indonesia

- 🇳🇬 Nigeria

The Royal Saudi Air Force’s Wing Loong II fleet alone logged 5,000 flight hours in 2024[5], demonstrating operational maturity and customer satisfaction. Military aviation researchers note that Chinese drone capabilities are narrowing the gap with Western competitors while maintaining significantly lower costs, making them increasingly competitive in export markets[5].

Naval Stealth Drone Deployment

The PLA’s newest amphibious assault vessel is equipped with up to six GJ-21 naval stealth drones, featuring a hybrid electric/gas engine system that enables extended operational range and short takeoff/landing (STOL) capabilities[6]. These drones reportedly carry up to 1,000 kilograms, have a flight range of 1,600 kilometers, and can operate from improvised surfaces like grass or dirt[6].

The GJ-21’s specifications suggest private sector involvement in critical subsystems. The hybrid propulsion technology, advanced composite materials, and autonomous navigation systems likely incorporate components and expertise from commercial drone manufacturers who have refined these technologies in civilian applications before adapting them for military use.

This dual-use technology transfer—where innovations flow between commercial and military applications—accelerates development in both sectors. Private companies gain access to military research funding and demanding performance requirements, while state programs benefit from the rapid iteration cycles and cost discipline that characterize private sector development.

Commercial Space: The New Frontier for Private Competition

While drones dominate current headlines, China’s commercial space sector represents the next frontier where private companies are challenging state dominance. Companies like LandSpace and iSpace are developing reusable rocket technology that could dramatically reduce launch costs and enable new space-based services.

Reusable Rocket Race

LandSpace’s Zhuque-3 reusable rocket program aims to compete directly with SpaceX’s Falcon 9, using methane-fueled engines that offer better performance and reusability than traditional kerosene-based systems. While still in development, the Zhuque-3 represents China’s most ambitious private space venture to date.

The commercial space sector differs from drones in several critical ways:

Higher capital requirements – Rocket development requires hundreds of millions in investment, limiting the field to well-funded startups and established aerospace companies.

Longer development cycles – From concept to first launch typically takes 5-7 years, compared to 12-24 months for new drone models.

Greater regulatory oversight – Space launches require extensive government approval and coordination, giving state programs more influence over private sector activities.

Strategic importance – Space capabilities have direct military applications, making the sector more sensitive to national security considerations.

Despite these challenges, private Chinese space companies have made remarkable progress. They benefit from government support for commercial space development, access to experienced aerospace engineers from state programs, and the same supply chain advantages that benefit drone manufacturers.

Regulatory Evolution and Market Consolidation

The regulatory framework governing China’s drone and commercial space race is evolving rapidly, with significant implications for how private companies compete with state programs. The July 2026 CAAC certification requirements represent the most significant regulatory shift in the industry’s history[1].

What the New Rules Mean

Starting in July 2026, all drone operations must comply with:

✅ Design certification – Proving airworthiness through rigorous testing

✅ Manufacturing standards – Demonstrating quality control and traceability

✅ Operational approval – Obtaining permits for specific use cases and geographic areas

✅ Electronic identification – Installing mandatory tracking systems for all commercial drones

These requirements serve multiple purposes. They improve safety and traceability, reducing accidents and enabling rapid response when problems occur. They also create market entry barriers that favor established players with resources to navigate complex compliance processes.

For private companies, the regulatory evolution presents both opportunities and challenges. Established firms like DJI, XAG, and EHang possess the financial resources and technical expertise to meet certification requirements, potentially strengthening their market positions. Smaller startups and new entrants face higher hurdles, potentially slowing innovation and reducing competitive pressure.

However, formalized regulations also create legitimacy and international recognition for Chinese drone systems. Countries considering Chinese drone imports often cite regulatory uncertainty as a concern. CAAC certification provides an official quality standard that can facilitate international sales and partnerships.

International Competitiveness and Geopolitical Challenges

As Chinese private companies expand globally, they encounter a complex landscape of geopolitical tensions, technology restrictions, and market access barriers. Understanding these challenges is essential for assessing the future trajectory of China’s drone and commercial space race.

The Protectionism Problem

Major markets including the United States and India have implemented or proposed restrictions on Chinese drone imports, citing national security concerns[4]. These measures include:

- 🚫 Import bans – Prohibiting government agencies from purchasing Chinese drones

- 🔒 Data security requirements – Mandating local data storage and processing

- 📋 Enhanced scrutiny – Subjecting Chinese drones to additional testing and certification

- 💼 Investment restrictions – Limiting Chinese companies’ ability to acquire Western drone manufacturers

These protectionist measures directly impact Chinese companies’ optimism about international expansion. Industry surveys show that Chinese drone firms’ outlook (6.2 on a 10-point scale) trails the global average (6.6), with geopolitical concerns cited as a primary factor[4].

Competitive Responses

Chinese private companies are adapting to these challenges through several strategies:

Geographic diversification – Focusing on markets in Southeast Asia, Middle East, Africa, and Latin America where geopolitical concerns are less pronounced and price sensitivity favors Chinese products.

Local partnerships – Establishing joint ventures and distribution agreements with local companies to reduce perceptions of Chinese control.

Technology localization – Offering customizable systems where sensitive components like data storage and processing can be provided by local suppliers.

Performance differentiation – Investing in capabilities that Western competitors cannot match at comparable price points, making Chinese systems indispensable despite geopolitical concerns.

The success of these strategies varies by market segment. Agricultural drones face fewer restrictions than surveillance systems, while commercial space launches encounter less scrutiny than military drones. Chinese companies are learning to navigate these complexities, tailoring their approach to each market’s specific concerns and opportunities.

The Role of Innovation Ecosystems

China’s success in drones and commercial space doesn’t stem solely from individual companies or government programs—it reflects the development of robust innovation ecosystems that connect research institutions, private companies, state programs, and venture capital.

Shenzhen: The Drone Capital

Shenzhen has emerged as the global center of drone innovation, hosting not only DJI but hundreds of component suppliers, software developers, and specialized service providers. This geographic concentration creates powerful network effects:

Knowledge spillovers – Engineers and executives move between companies, spreading expertise and best practices across the ecosystem.

Specialized suppliers – Component manufacturers develop products specifically for drone applications, reducing costs and improving performance.

Rapid prototyping – Proximity to manufacturing facilities enables quick iteration from design to production.

Venture capital concentration – Investors with drone expertise cluster in Shenzhen, providing funding and strategic guidance to startups.

This ecosystem approach mirrors Silicon Valley’s success in software and semiconductors, demonstrating that China has learned to cultivate innovation environments that foster both competition and collaboration.

University-Industry Partnerships

Leading Chinese universities including Tsinghua, Beihang, and Northwestern Polytechnical University maintain close relationships with both state aerospace programs and private drone companies. These partnerships facilitate:

- 🎓 Talent pipeline – Graduates with specialized aerospace and robotics training

- 🔬 Joint research – Collaborative projects addressing fundamental technical challenges

- 💡 Technology transfer – Moving innovations from academic labs to commercial products

- 📚 Continuing education – Keeping industry professionals current with latest developments

The integration of academic research, state programs, and private industry creates a virtuous cycle where each sector strengthens the others. This model contrasts with Western approaches that often maintain sharper boundaries between academic, government, and commercial research.

Future Outlook: Where Competition Is Heading

As we look beyond 2026, several trends will shape how China’s drone and commercial space race evolves and how private companies continue competing with state programs.

Emerging Technology Frontiers

Autonomous swarm systems – Multiple drones operating in coordination without human control, enabling applications from agricultural monitoring to logistics networks. Private companies are leading development due to their software expertise and agile development processes.

AI-powered decision-making – Advanced artificial intelligence that enables drones to respond to complex, unpredictable situations without pre-programmed instructions. This capability is critical for applications like emergency response and infrastructure inspection.

Extended range and endurance – New battery technologies and hybrid propulsion systems that enable multi-hour flights and hundreds of kilometers range. These improvements unlock applications currently limited by short flight times.

Urban air mobility – Passenger-carrying eVTOL aircraft that could transform urban transportation. While still in early stages, companies like EHang are conducting trials that could lead to commercial operations within 3-5 years[4].

Market Consolidation vs. Continued Fragmentation

The industry faces a fundamental question: Will it consolidate around a few dominant players, or will specialized niches support continued fragmentation?

Arguments for consolidation include:

- Rising regulatory compliance costs favoring large companies

- Network effects in software platforms creating winner-take-all dynamics

- Economies of scale in manufacturing reducing unit costs for high-volume producers

- Customer preference for established brands with proven reliability

Arguments for continued fragmentation include:

- Diverse application requirements preventing one-size-fits-all solutions

- Rapid technological change creating opportunities for innovative entrants

- Geographic and regulatory barriers limiting global consolidation

- Government policies supporting multiple domestic champions

The most likely outcome involves consolidation in high-volume consumer segments (where DJI’s dominance may strengthen) alongside continued fragmentation in specialized industrial and military applications (where customization and niche expertise matter more than scale).

International Expansion Trajectories

Chinese private companies’ international success will largely depend on their ability to navigate geopolitical challenges while maintaining cost and performance advantages. Key factors include:

Technology sovereignty concerns – As more countries develop policies around critical technology supply chains, Chinese companies may face growing restrictions in Western markets while finding greater acceptance in developing economies.

Local manufacturing – Establishing production facilities outside China could help companies overcome import restrictions and address data security concerns, though it may reduce cost advantages.

Standards and certification – Active participation in international standards bodies could help Chinese companies shape global regulations rather than simply responding to them.

Brand development – Moving beyond price competition to build premium brands associated with innovation and quality, similar to how Japanese and Korean companies evolved.

Conclusion: A New Model of Public-Private Competition

China’s drone and commercial space race demonstrates a distinctive model where private companies compete with state programs while simultaneously collaborating with them. This approach differs fundamentally from both the purely commercial Western model and the state-dominated systems of earlier Chinese industrial development.

The results speak for themselves: China operates over 300,000 agricultural drones (60%+ of the global total), projects a RMB 3.5 trillion low-altitude economy by 2035, and has created multiple globally competitive private companies in less than a decade[1][3]. Private firms like DJI, XAG, EHang, and Aerospace Times Feipeng have achieved success not despite state involvement but partly because of it—benefiting from supportive policies, infrastructure investment, and access to military-civilian technology transfer.

As this industry matures, several actionable insights emerge for stakeholders:

For policymakers: The Chinese model demonstrates that government support and private competition can coexist productively. Strategic infrastructure investment, clear regulatory frameworks, and support for innovation ecosystems enable private sector success without requiring direct state ownership.

For companies: Success in China’s competitive environment requires continuous innovation, cost discipline, and strategic positioning. International expansion demands careful navigation of geopolitical challenges and adaptation to local market requirements.

For investors: The drone and commercial space sectors offer significant growth opportunities, but require careful assessment of regulatory risks, competitive dynamics, and geopolitical factors that could impact returns.

For international competitors: Chinese companies’ cost advantages and rapid development cycles represent formidable competitive challenges. Western firms must differentiate through superior technology, trusted brands, or specialized capabilities that justify premium pricing.

The evolution of China’s drone and commercial space race will continue shaping global technology competition for years to come. As private companies push boundaries in automation, artificial intelligence, and aerospace engineering, they’re not just competing with state programs—they’re redefining what’s possible in unmanned systems and commercial space access. The question is no longer whether Chinese private companies can compete globally, but how quickly they’ll establish leadership in emerging technology sectors that will define the 21st century economy.

References

[1] Chinas Industries To Watch In 2026 – https://www.china-briefing.com/news/chinas-industries-to-watch-in-2026/

[2] Chinas Aerospace Times Feipeng Pushes Global Expansion As Domestic Drone Market Heats Up – https://moderndiplomacy.eu/2026/02/05/chinas-aerospace-times-feipeng-pushes-global-expansion-as-domestic-drone-market-heats-up/

[3] China Highlights Drones Robots Use In Top Annual Agriculture Policy Blueprint For First Time – https://www.yicaiglobal.com/news/china-highlights-drones-robots-use-in-top-annual-agriculture-policy-blueprint-for-first-time

[4] Drone Companies In The Chinese Drone Market – https://droneii.com/drone-companies-in-the-chinese-drone-market

[5] Chinas New Maritime Combat Drone Poised For Global Success Analysts – https://www.defensenews.com/global/asia-pacific/2026/02/12/chinas-new-maritime-combat-drone-poised-for-global-success-analysts/

[6] China Taiwan Update February 13 2026 – https://understandingwar.org/research/china-taiwan/china-taiwan-update-february-13-2026/

Some content and illustrations on GEORGIANBAYNEWS.COM are created with the assistance of AI tools.

GEORGIANBAYNEWS.COM shares video content from YouTube creators under fair use principles. We respect creators’ intellectual property and include direct links to their original videos, channels, and social media platforms whenever we feature their content. This practice supports creators by driving traffic to their platforms.

{kind=link}