The Ambassador: Why Are the Bond Markets 📉 Struggling in 2026?

Sharing is SO MUCH APPRECIATED!

Last updated: May 23, 2026

Quick Answer: Bond markets are struggling because interest rates have stayed elevated for an extended period, eroding the value of existing bonds and shaking investor confidence. When rates rise, bond prices fall — and that inverse relationship has punished bondholders across government, corporate, and municipal debt categories. The pressure is compounded by persistent inflation concerns, heavy government borrowing, and growing uncertainty about central bank policy direction.

Key Takeaways

- Bond prices move opposite to interest rates — when rates go up, existing bond values fall.

- The U.S. Federal Reserve and Bank of Canada kept benchmark rates at multi-decade highs well into 2025, dragging bond portfolios down.

- Long-duration bonds (10–30 year maturities) have suffered the steepest losses.

- Government bonds are still relatively safer than corporate bonds, but neither category has been immune.

- Retirement savers with heavy bond allocations have seen real purchasing power erode.

- Short-term bonds and Treasury bills have held up better than long-term debt.

- Investors can reduce risk by shortening bond duration or diversifying into alternatives.

- The bond market’s struggles also affect mortgage rates, corporate borrowing costs, and real estate values.

What Exactly Is Happening in Bond Markets Right Now?

Bond markets are struggling under the weight of sustained high interest rates, elevated government debt issuance, and fragile investor confidence. In simple terms: governments and corporations issue bonds to borrow money, and when the cost of borrowing rises, the value of older, lower-yielding bonds drops.

Here’s the core dynamic playing out in 2026:

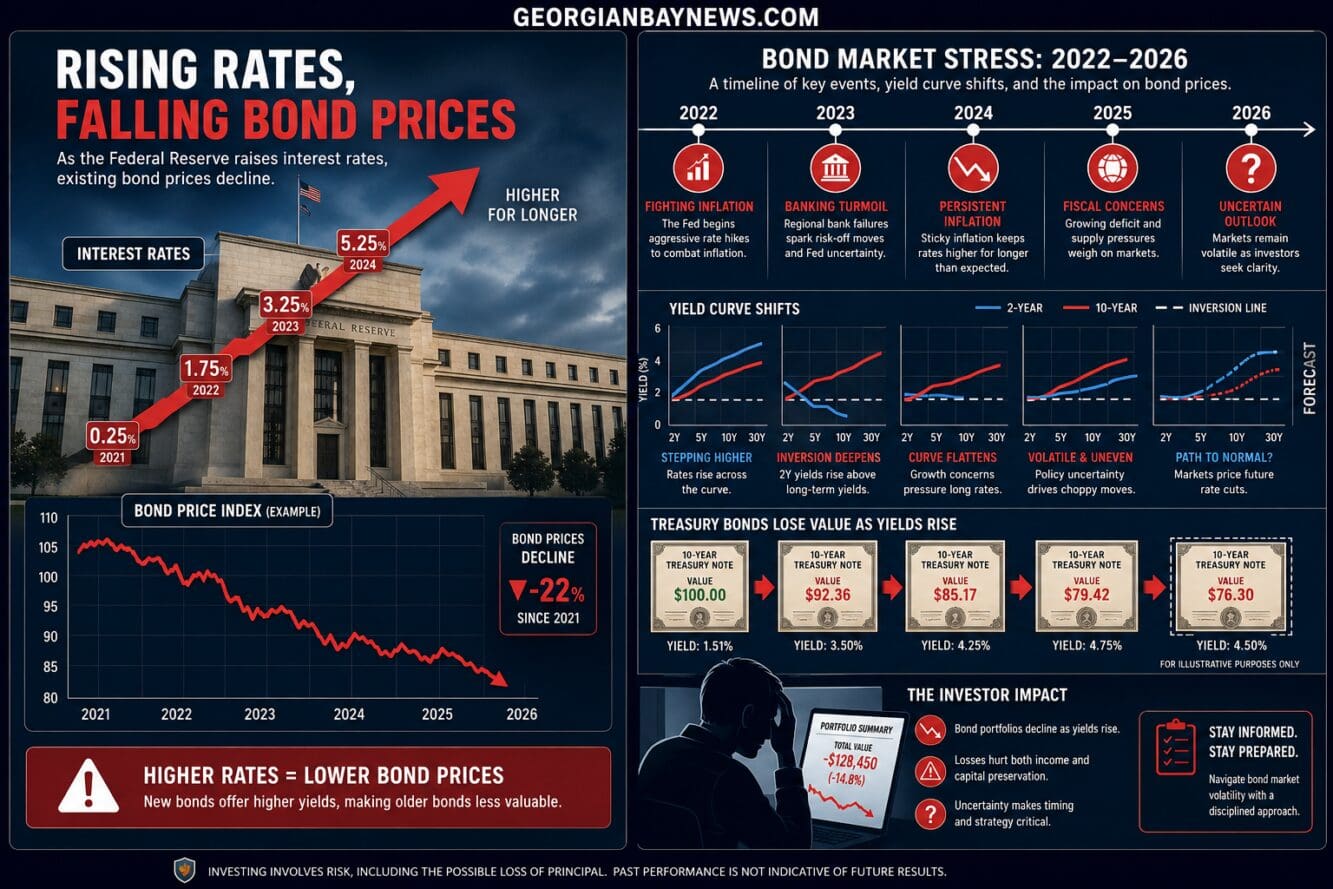

- Central banks in the U.S., Canada, and the U.K. raised rates aggressively starting in 2022 to fight inflation (U.S. Federal Reserve data, 2022–2024).

- Even as some rate cuts began in late 2024 and 2025, rates remain historically elevated.

- Government bond supply has surged as deficits widened, flooding the market with new debt and pushing yields higher.

- Investor demand has softened, particularly from foreign buyers who once absorbed large portions of U.S. Treasury issuance.

“The bond market is the world’s largest financial market — when it struggles, the ripple effects touch everything from mortgages to retirement accounts.”

The result is a market where bond yields are high but bond prices are low, leaving many existing bondholders sitting on paper losses.

How Are Rising Interest Rates Affecting Bond Prices?

Rising interest rates are the single biggest reason bond markets are struggling. When new bonds are issued at higher yields, older bonds paying lower rates become less attractive — so their market price falls to compensate.

A simple example:

- You hold a 10-year Treasury bond paying 2% annually.

- New 10-year Treasuries now yield 4.5%.

- No one will pay full price for your 2% bond, so its market value drops significantly.

This isn’t a glitch — it’s how bond math works. The longer the bond’s maturity, the more sensitive it is to rate changes. A 30-year bond can lose 20–30% of its value when rates rise by 2 percentage points (a standard duration calculation used by fixed-income analysts).

Common mistake: Many investors assumed bonds were “safe” and didn’t account for interest rate risk. Bonds carry low default risk but significant price risk when rates move sharply.

Why Are Treasury Bonds Losing Value?

Treasury bonds are losing value for three overlapping reasons: rate sensitivity, rising supply, and weakening demand. Even though U.S. Treasuries carry no default risk (the U.S. government can always print dollars), they are not immune to price declines driven by rate changes.

Key factors specific to Treasuries:

- Massive deficit spending has required the U.S. Treasury to issue record volumes of new bonds, increasing supply.

- Foreign central banks (notably China and Japan) have reduced their Treasury holdings, shrinking a key buyer base (U.S. Treasury TIC data, 2023–2024).

- Inflation uncertainty has kept long-term yields elevated, as investors demand higher compensation for holding long-duration debt.

For Canadian readers concerned about similar dynamics, the Southern Georgian Bay real estate market has also felt the squeeze of elevated bond yields through higher mortgage rates — a direct transmission channel from bond markets to everyday finances.

How Do Current Bond Market Conditions Compare to Past Downturns?

The current bond market struggle is historically unusual in both speed and scale. For context:

PeriodTrigger10-Year Treasury Peak YieldDuration of Stress1994Fed tightening cycle~8%~12 months2013″Taper Tantrum”~3%~6 months2022–2025Post-pandemic inflation~5%3+ years

The 2022–2025 cycle has been the most damaging for bond portfolios since the early 1980s, when the Fed under Paul Volcker raised rates to break inflation (Federal Reserve historical data). What makes the current period different is the duration of stress — prolonged elevated rates have prevented the recovery bounce that typically follows a rate shock.

Which Types of Bonds Are Most at Risk?

Not all bonds suffer equally. Long-duration and lower-quality bonds face the greatest pressure when bond markets are struggling.

Highest risk:

- Long-term government bonds (20–30 year maturities) — most sensitive to rate changes.

- High-yield (junk) corporate bonds — face both rate risk and credit risk if the economy slows.

- Emerging market bonds — exposed to currency risk on top of rate pressure.

Lower risk (relatively):

- Short-term T-bills (under 1 year) — mature quickly, so price impact is minimal.

- Floating-rate bonds — their coupon payments adjust with rates.

- Inflation-linked bonds (TIPS, RRBs) — offer partial protection against inflation erosion.

Choose long-duration bonds only if you believe rates will fall significantly and soon. Choose short-duration bonds if rate uncertainty remains high.

How Are Corporate Bonds Different From Treasury Bonds During Market Stress?

Corporate bonds carry an additional layer of risk compared to Treasuries: credit risk, meaning the issuer could default. During market stress, this spread widens.

- Investment-grade corporate bonds track Treasury yields closely but add a “credit spread” of 1–2 percentage points (typical range, Bloomberg data).

- High-yield corporate bonds can see spreads blow out to 5–8 points or more during recessions, compounding losses.

- When economic growth slows alongside high rates, corporate bonds face a double threat: falling prices and rising default risk.

For investors building stronger bonds in their portfolios, understanding the credit quality of holdings is as important as understanding duration.

Are Government Bonds Still a Safe Investment?

Government bonds from stable economies (U.S., Canada, U.K., Germany) remain among the safest assets for default risk — but they are not safe from price risk in a rising-rate environment. The distinction matters.

If you hold a government bond to maturity, you will receive all promised payments. If you need to sell before maturity, you may sell at a loss. For long-term investors who don’t need liquidity, government bonds still serve their core purpose. For those who might need to access funds, short-term government bonds or money market funds are safer alternatives right now.

What Should Investors Do If Their Bond Portfolio Is Tanking?

Bond markets struggling doesn’t mean investors are helpless. There are concrete steps to reduce damage and reposition.

Actionable steps:

- Shorten duration — Shift from long-term to short-term bonds to reduce price sensitivity.

- Review credit quality — Trim high-yield exposure if a recession looks likely.

- Consider TIPS or RRBs — Inflation-linked bonds protect purchasing power.

- Don’t panic-sell — If you can hold to maturity, paper losses don’t become real losses.

- Rebalance gradually — Move a portion into alternatives (see below) rather than abandoning bonds entirely.

- Ladder your bonds — Hold bonds maturing at different dates so you’re not locked into any single rate environment.

Staying informed about states of emergency in economic policy — like sudden central bank pivots — can help investors react faster when conditions shift.

What Mistakes Are Investors Making in This Bond Market Downturn?

Several predictable errors are amplifying losses for individual investors.

- Chasing yield without checking duration: Buying long-term bonds because yields look attractive, without understanding the price risk if rates stay high.

- Treating all bonds as “safe”: Conflating low default risk with low price risk.

- Panic selling at the bottom: Locking in losses right before a potential rate-cut recovery.

- Ignoring inflation: Even if a bond pays 4%, a 3.5% inflation rate leaves real returns thin.

- Over-concentration: Holding 60–70% of a portfolio in bonds during a prolonged rate-hike cycle without any short-duration or alternative exposure.

Understanding stress in financial markets — and separating short-term noise from structural shifts — is a skill that separates reactive investors from resilient ones.

How Do Bond Market Struggles Impact Retirement Savings?

Bond markets struggling directly harm retirement savers, particularly those in or near retirement who rely on bonds for stability and income.

- Target-date funds automatically shift toward bonds as retirement approaches — those nearing retirement in 2022–2025 saw significant drawdowns.

- Defined benefit pension plans use bond yields to calculate future liabilities; rising yields can actually improve pension funding ratios, a counterintuitive silver lining.

- RRSP and 401(k) holders with bond ETF exposure have seen real portfolio value decline.

- Sequence-of-returns risk is heightened: withdrawing from a portfolio during a bond drawdown locks in losses permanently.

For those in communities like South Georgian Bay and across Canada, where many retirees rely on fixed-income portfolios, the practical impact of bond market volatility is very real.

Can Small Investors Protect Themselves From Bond Market Volatility?

Small investors have more tools available than many realize. Protection doesn’t require complex derivatives or institutional access.

Practical options for everyday investors:

- GICs and CDs: Guaranteed Investment Certificates (Canada) or Certificates of Deposit (U.S.) lock in current high rates with no price risk.

- Short-term bond ETFs: Funds like those holding 1–3 year maturities limit duration risk significantly.

- High-interest savings accounts: Offer competitive yields without any bond price exposure.

- Bond ladders: Spread maturities across 1, 3, 5, and 7 years so you always have bonds coming due for reinvestment.

- I-Bonds (U.S.): Inflation-adjusted savings bonds with purchase limits but strong protection.

The key insight: small investors don’t need to predict where rates go — they need to structure their fixed-income holdings so they’re not forced to sell at a loss.

What Alternatives Exist If Bonds Aren’t Performing?

When bond markets are struggling, several asset classes can fill the income and stability role that bonds traditionally play.

AlternativeIncome PotentialRisk LevelLiquidityDividend stocksModerate–HighMediumHighREITsModerateMedium–HighHighGICs / CDsModerateVery LowLow–MediumInfrastructure fundsModerateMediumMediumPreferred sharesModerateMediumHighMoney market fundsLow–ModerateVery LowVery High

Choose dividend stocks if you can tolerate equity volatility and want inflation-linked income growth. Choose GICs or money market funds if capital preservation is the priority. REITs are sensitive to interest rates too, so they’re not a perfect substitute during rate stress.

For readers tracking broader economic trends in Southern Georgian Bay communities, understanding how bond market conditions filter into local real estate and business borrowing costs adds important context to these investment decisions.

Will Bond Market Losses Continue in 2026?

The outlook for bond markets in 2026 is cautiously mixed. Rate cuts from the U.S. Federal Reserve and Bank of Canada that began in late 2024 have provided some relief, but the pace of cuts has been slower than markets anticipated.

Factors that could improve bond markets:

- Further central bank rate cuts as inflation continues to moderate.

- Slower economic growth reducing inflationary pressure.

- Reduced government deficit spending easing bond supply pressure.

Factors that could keep bond markets struggling:

- Inflation re-accelerating due to trade policy or energy price shocks.

- Governments continuing to run large deficits, flooding markets with new bonds.

- Central banks pausing or reversing rate cuts if inflation proves sticky.

Most fixed-income analysts (as of early 2026) expect gradual improvement in bond prices as rates drift lower, but a return to the ultra-low-yield era of 2015–2021 is considered unlikely in the near term.

FAQ

Q: Why do bond prices fall when interest rates rise?

When rates rise, newly issued bonds offer higher yields, making existing lower-yield bonds less valuable. Investors discount the older bond’s price until its effective yield matches the market rate.

Q: Are short-term bonds safer than long-term bonds right now?

Yes. Short-term bonds mature quickly, so their prices are far less sensitive to rate changes. In a high-rate environment, short-duration bonds carry significantly lower price risk.

Q: Should I sell my bond funds now?

Not necessarily. Selling locks in losses. If you can hold to maturity (or hold a fund long-term), prices typically recover as rates stabilize or fall. Reassess your duration exposure rather than exiting entirely.

Q: How long does a bond market downturn typically last?

Historical downturns have lasted 6 to 18 months in most cycles. The current cycle (2022–2025+) has been unusually prolonged due to persistent inflation and heavy government borrowing.

Q: Are Canadian bonds safer than U.S. bonds right now?

Both carry negligible default risk. Canadian bonds have faced similar pressures from Bank of Canada rate hikes, though Canada’s fiscal position and debt levels differ from the U.S. Neither is dramatically safer in price-risk terms.

Q: What is a bond yield, and why does it matter?

A bond yield is the annual return an investor earns, expressed as a percentage of the bond’s current price. Higher yields mean lower prices. Yields are the primary signal of bond market health.

Q: Can bonds recover if inflation drops?

Yes. If inflation falls and central banks cut rates, bond prices rise. A meaningful drop in inflation is the most reliable catalyst for a bond market recovery.

Q: What is duration risk?

Duration measures how sensitive a bond’s price is to interest rate changes. A bond with a duration of 10 years will lose roughly 10% of its value for every 1% rise in rates.

Q: Are I-Bonds a good alternative to regular bonds?

U.S. I-Bonds offer inflation-adjusted returns and no price risk, but purchases are capped at $10,000 per person per year. They’re a useful tool but can’t replace a full bond allocation.

Q: How do bond market struggles affect mortgage rates?

Mortgage rates are closely tied to 10-year Treasury yields. When bond yields rise, mortgage rates follow — which is why home affordability has tightened alongside bond market stress.

Conclusion: What to Do Next

Bond markets struggling is not a temporary blip — it reflects a structural shift in the interest rate environment that has been building since 2022. The good news: investors who understand the mechanics have clear options.

Actionable next steps:

- Audit your bond holdings — check the average duration of your bond funds and consider whether it matches your time horizon.

- Shorten duration if needed — move toward short-term bond ETFs, GICs, or money market funds if you need stability.

- Don’t abandon bonds entirely — they still provide diversification and will recover value as rates eventually fall.

- Explore income alternatives — dividend stocks, REITs, and preferred shares can complement a reduced bond allocation.

- Stay informed — central bank decisions in the next 12 months will be the biggest driver of bond market direction.

The bond market’s struggles are painful, but they’re also creating opportunities for investors willing to buy bonds at yields not seen in over a decade. Patience, diversification, and duration management are the tools that matter most right now.

References

- U.S. Federal Reserve — Federal Funds Rate historical data. federalreserve.gov (2022–2024)

- U.S. Department of the Treasury — Treasury International Capital (TIC) System data. treasury.gov (2023–2024)

- Bloomberg Fixed Income Research — Investment-grade and high-yield credit spread data. bloomberg.com (2023–2024)

- Bank of Canada — Policy interest rate decisions and monetary policy reports. bankofcanada.ca (2022–2025)

Content, illustrations, and third-party video appearing on GEORGIANBAYNEWS.COM may be generated or curated with AI assistance or reproduced pursuant to the fair dealing provisions of the Copyright Act, R.S.C. 1985, c. C-42. Attribution and hyperlinks to original sources are provided in acknowledgment of applicable intellectual property rights. Such referencing is intended to direct traffic to and support the original rights holders’ platforms.

Sharing is SO MUCH APPRECIATED!

{kind=link}