Bank of Canada Holds Interest Rates Steady: Inflation Outlook, Housing Market Ripple Effects, and Borrower Next Steps

Canada’s central bank has once again chosen to stay the course. On March 18, 2026, the Bank of Canada held its overnight target rate at 2.25%, keeping the Bank Rate at 2.5% and the deposit rate at 2.20% [3]. This marks the third consecutive hold since the last rate cut in October 2025—and it sends a clear message to borrowers, homebuyers, and savers alike: patience is still the name of the game. With oil shocks rattling global markets, a softening labor market, and housing still stuck in neutral, understanding the full picture behind the Bank of Canada holds interest rates steady decision is essential for anyone planning their next financial move.

Key Takeaways 📌

- Rate unchanged at 2.25%: The Bank of Canada held steady for the third consecutive announcement, citing elevated uncertainty and an appropriate current policy stance [3].

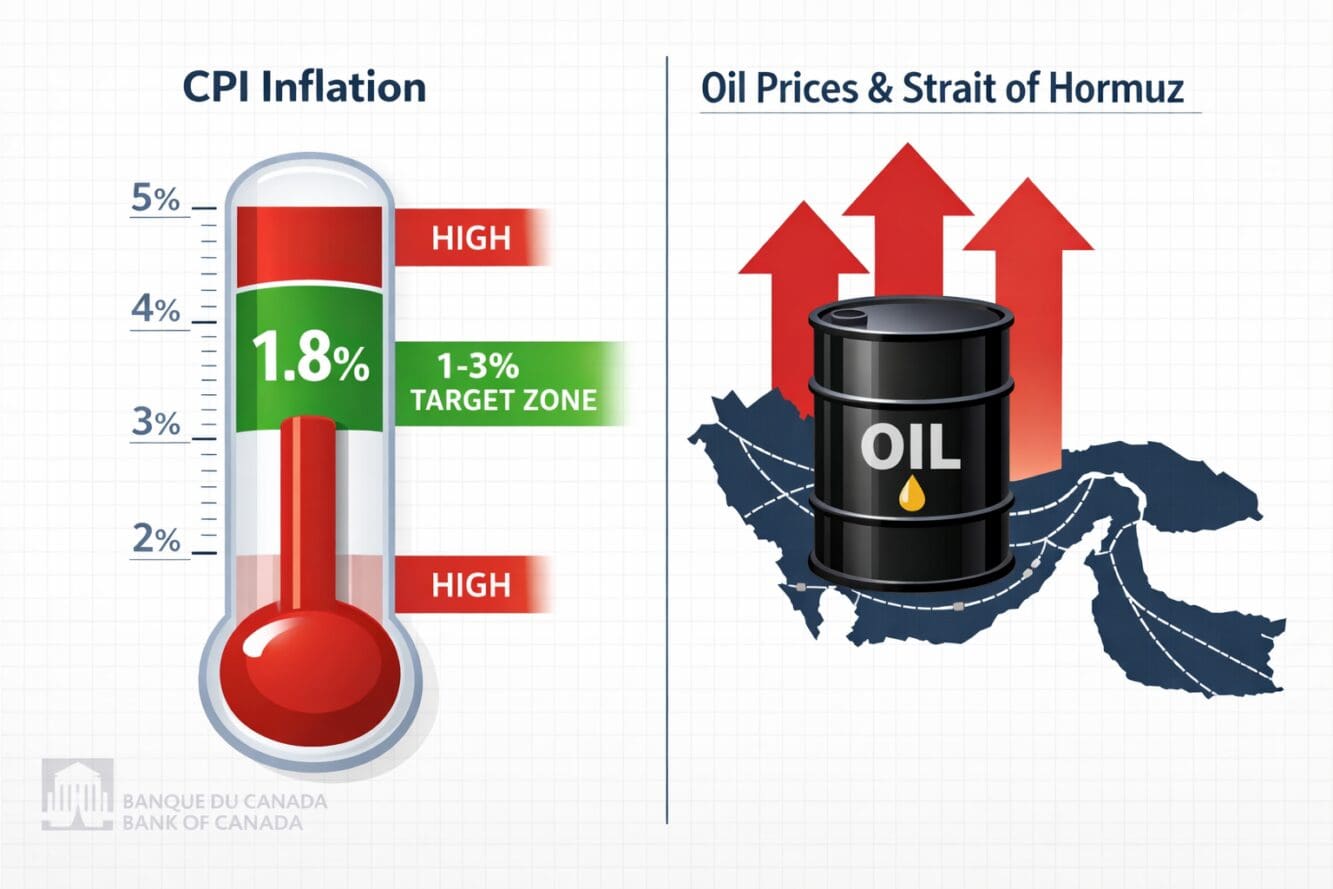

- Inflation cooling but fragile: CPI inflation dropped to 1.8% in February 2026, but rising global energy prices could push it higher in coming months [3][4].

- GDP contracted in late 2025: The economy shrank by 0.6% in Q4 2025, and the unemployment rate climbed to 6.7% in February 2026 [3].

- Housing market remains weak: Despite strong domestic demand, housing activity has not recovered, delaying mortgage relief for many Canadians [3].

- No rate hike—yet: Markets and economists expect the BoC to stay on the sidelines, but a rate hike is possible if inflation pressures broaden [1][4].

Why the Bank of Canada Holds Interest Rates Steady: Inflation Outlook, Housing Market Ripple Effects, and Borrower Next Steps Explained

The decision to hold rates was widely expected. Market analysts had priced in a hold well before the announcement, and TD Economist Maria Solovieva confirmed that with inflation sitting within the BoC’s 1–3% target band and GDP growth in a reasonable range, there was “no strong reason to change course” [1][2].

But “no change” doesn’t mean “no worries.” The BoC acknowledged that uncertainty has increased significantly since its January announcement. Three forces are colliding:

- Global oil shocks from the ongoing Middle East conflict

- U.S. trade policy uncertainty and tariff threats

- A softening domestic labor market with rising unemployment

The Bank stated plainly that “current policy remains appropriate given the Bank’s baseline economic outlook” [3]. Translation? Rates aren’t moving until the fog clears.

The Inflation Picture: Cooling Numbers, Heating Risks 🔥

February’s Good News

On the surface, the inflation data looks encouraging. CPI inflation eased to 1.8% in February 2026, down from 2.3% in January [3]. Core inflation measures also hovered near the 2% target—right where the BoC wants them.

Food inflation, while still elevated, showed signs of slowing. For Canadian families feeling the pinch at the grocery store, this offered a small but welcome reprieve.

The Oil Shock Wild Card

Here’s where things get complicated. The Middle East conflict has sent global energy prices surging, and the threat to the Strait of Hormuz—through which roughly 20% of the world’s oil supply passes—has created serious supply concerns [4].

💡 “The supply shock could easily escalate, broadening inflation beyond energy prices.” — TD Bank analysis [4]

Higher oil prices mean higher gasoline costs for Canadians. But the ripple effects go further. The Strait of Hormuz bottleneck also threatens fertilizer supply chains, which could push food prices back up just as they were cooling [4]. For communities already dealing with rising costs, this is a concern worth watching closely. Organizations focused on community support and rehousing know firsthand how inflation hits vulnerable populations hardest.

| Inflation Indicator | January 2026 | February 2026 | Trend |

|---|---|---|---|

| CPI (headline) | 2.3% | 1.8% | ⬇️ Declining |

| Core inflation | ~2.1% | ~2.0% | ➡️ Stable |

| Food inflation | Elevated | Slowing | ⬇️ Improving |

| Energy prices | Rising | Rising sharply | ⬆️ Concerning |

GDP and Jobs: A Mixed Economic Report Card 📊

Economic Contraction in Late 2025

The Canadian economy contracted by 0.6% in Q4 2025—weaker than most forecasts predicted [3]. The main culprit was a larger-than-expected inventory drawdown. However, underneath that headline number, domestic demand actually grew by more than 2%, driven by consumer and government spending.

This creates a confusing picture: Canadians are spending, but the broader economy is shrinking.

The Labor Market Softens

Perhaps more concerning is the unemployment rate, which rose to 6.7% in February 2026 [3]. Employment gains from late 2025 were largely reversed in the first two months of 2026.

For Ontario in particular—where manufacturing and trade-sensitive sectors are concentrated—the combination of U.S. tariff uncertainty and a cooling job market creates real anxiety. Workers in regions dependent on cross-border trade may feel the effects most acutely. Those exploring alternative housing solutions like tiny homes are finding creative ways to reduce living costs during uncertain times.

Housing Market Ripple Effects: Why Mortgage Relief Is Delayed 🏠

Still Waiting for a Rebound

Despite the rate cuts of 2025, housing markets remain weak across Canada [3]. The BoC explicitly noted this weakness even as overall domestic demand showed strength.

Why hasn’t housing bounced back? Several factors are at play:

- Affordability remains stretched even at lower rates

- Population growth has slowed, reducing demand pressure

- Buyer confidence is low amid economic uncertainty

- Mortgage stress test rules still limit borrowing capacity

What This Means for Homeowners and Buyers

For homeowners hoping for another rate cut to ease their mortgage payments, the hold means relief is on pause. Variable-rate mortgage holders will see no change to their payments, while those renewing fixed-rate mortgages may find rates slightly lower than their original terms—but not dramatically so.

For prospective buyers, the silver lining is that a stable rate environment provides predictability. There’s no urgency to rush into a purchase before rates drop further, but there’s also no reason to fear sudden rate hikes—at least not yet.

Communities investing in long-term infrastructure and asset management are taking a similarly measured approach to planning amid uncertainty.

Could Rates Actually Go Up? The Hike Scenario 📈

While the base case is for rates to hold steady through mid-2026, markets have not ruled out a potential rate hike later in the year [1].

What would trigger a hike? According to TD Bank’s analysis, the BoC would need to see:

- ✅ Persistent, broadening inflation beyond energy prices

- ✅ Rising consumer inflation expectations becoming entrenched

- ✅ Evidence that supply shocks are feeding into core prices

TD Bank expects the BoC to “stay on the sidelines for now” but cautioned that the situation could change quickly if oil prices continue climbing [4]. For savers and investors, this means locking in GIC rates or high-interest savings accounts now could be a smart move while yields remain attractive.

Borrower Next Steps: Practical Advice for 2026 💰

For Variable-Rate Mortgage Holders

Your rate isn’t changing today, but stay alert. If oil shocks push inflation higher, a rate hike could follow. Consider:

- Stress-testing your budget at a rate 0.50–0.75% higher

- Building an emergency fund equal to 3–6 months of expenses

- Speaking with your lender about conversion options to fixed rates

For Fixed-Rate Mortgage Renewals

If your mortgage is up for renewal in 2026, you’re likely renewing at a lower rate than your original term. Shop around—don’t just accept your lender’s first offer. Even small differences in rate can save thousands over a five-year term.

For Savers and Investors

The hold at 2.25% keeps savings account and GIC yields relatively stable. This is a good time to:

- Lock in 1–2 year GICs while rates are still favorable

- Diversify investments to hedge against inflation risk

- Avoid panic moves—the BoC is signaling stability, not crisis

For those looking at broader financial literacy and understanding how global economic forces shape daily life, staying informed is the best investment of all.

For Prospective Homebuyers

The rate hold gives you breathing room. Use this time to:

- Get pre-approved to understand your true buying power

- Research regional markets—some areas offer better value

- Watch the April BoC announcement (April 16, 2026) for updated guidance

Those considering community-oriented developments and public input opportunities should stay engaged with local planning processes that affect housing supply.

What to Watch Next 👀

The Bank of Canada’s next interest rate announcement is scheduled for April 16, 2026 [6]. By then, the BoC will have updated economic projections and more data on whether oil price increases are bleeding into broader inflation.

Key indicators to monitor:

| What to Watch | Why It Matters |

|---|---|

| March CPI report | Will inflation stay below 2% or rebound? |

| Employment data | Is the 6.7% unemployment rate a trend? |

| Oil prices | Strait of Hormuz developments are critical |

| U.S. tariff announcements | Trade policy directly impacts Canadian GDP |

| Housing starts | Any sign of recovery in residential construction? |

For communities tracking severe weather and infrastructure resilience, economic stability and preparedness go hand in hand.

Conclusion

The Bank of Canada’s decision to hold interest rates steady at 2.25% reflects a central bank navigating between cooling inflation and rising global risks. While February’s 1.8% CPI reading was encouraging, the threat of oil shocks, a softening labor market, and persistent housing weakness mean the BoC is right to proceed with caution.

Here are your actionable next steps:

- 📋 Review your mortgage terms and stress-test your budget for potential rate changes

- 💵 Lock in savings rates while GIC yields remain attractive

- 🏠 Don’t rush into housing decisions—stability gives you time to plan

- 📰 Mark April 16, 2026 on your calendar for the next BoC rate announcement

- 🌍 Monitor global oil prices—they’re the biggest wildcard for Canadian inflation in 2026

The Bank of Canada holds interest rates steady for now, but the road ahead is anything but certain. Stay informed, stay prepared, and make your financial decisions based on data—not fear.

References

[1] Bank Of Canada Interest Rate March 2026 – https://stories.td.com/ca/en/article/bank-of-canada-interest-rate-march-2026

[2] Interest Rate – https://tradingeconomics.com/canada/interest-rate

[3] Fad Press Release 2026 03 18 – https://www.bankofcanada.ca/2026/03/fad-press-release-2026-03-18/

[4] Bank Of Canada Rate Announcement March 2026 – https://globalnews.ca/news/11735955/bank-of-canada-rate-announcement-march-2026/

[6] Key Interest Rate – https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

Content, illustrations, and third-party video appearing on GEORGIANBAYNEWS.COM may be generated or curated with AI assistance or reproduced pursuant to the fair dealing provisions of the Copyright Act, R.S.C. 1985, c. C-42. Attribution and hyperlinks to original sources are provided in acknowledgment of applicable intellectual property rights. Such referencing is intended to direct traffic to and support the original rights holders’ platforms.

{kind=link}