Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026

Sharing is SO MUCH APPRECIATED!

The world’s most powerful nations are locked in an unprecedented struggle—not over oil or traditional commodities, but over rare earths and critical minerals that power everything from smartphones to fighter jets. As 2026 unfolds, Rare Earths and Critical Minerals has become the defining geopolitical contest of our era, with the United States, China, and emerging players like Canada racing to secure supply chains that will determine economic and military dominance for decades to come.

This isn’t just about mining rocks from the ground. It’s about controlling the essential building blocks of modern civilization—the elements that make electric vehicles run, wind turbines spin, and defense systems operate. With China wielding rare earths as economic weapons and Western nations scrambling to build alternative supply chains, the stakes have never been higher.

Key Takeaways

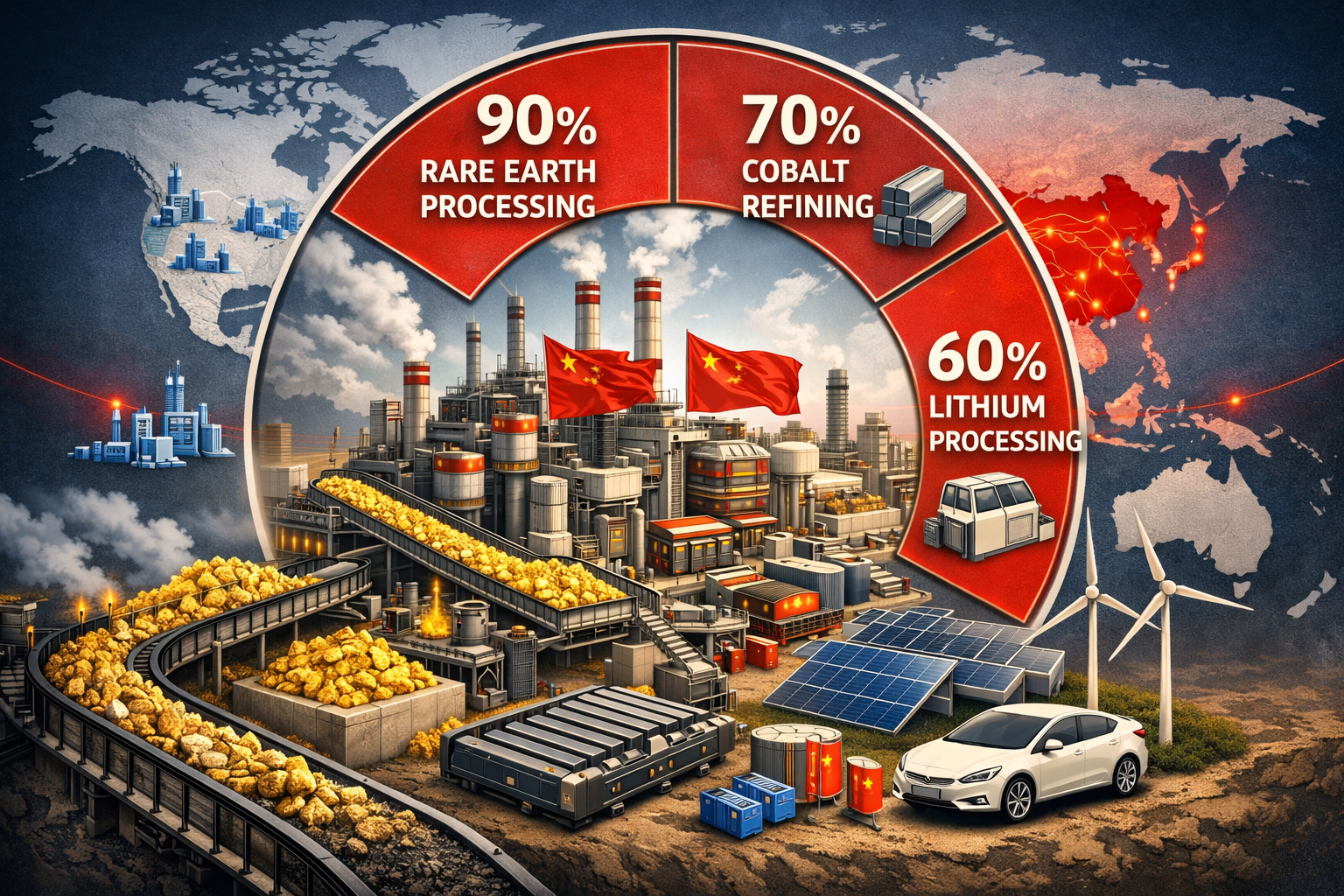

- 🌍 China dominates 90% of global rare earth processing, giving Beijing unprecedented leverage over Western technology and defense industries

- 💰 The US has committed $12 billion to a critical mineral stockpile while backing Brazil’s rare earth production with $565 million to break Chinese supply chain control

- 🤝 54 countries convened for coordinated strategy, with the US signing 11 new bilateral mineral accords including a $1 billion US-Australia partnership

- ⚠️ China weaponized rare earth exports in January 2026, restricting shipments to Japan and forcing European automakers to halt production

- 🇨🇦 Canada is emerging as a critical supplier, nearing a $3 billion uranium deal with India and positioning itself as a secure alternative to Chinese dominance

Understanding the Critical Minerals Crisis

Critical minerals are elements essential for modern technology and national security that face supply chain vulnerabilities. This category includes rare earth elements (17 metallic elements), lithium, cobalt, gallium, antimony, and others that power renewable energy systems, consumer electronics, and military hardware.

The crisis stems from a dangerous concentration of production. Chinese state-owned companies control not just extraction, but crucially, the processing and refining that transforms raw ore into usable materials. This downstream dominance gives Beijing control over manufacturing of:

- ⚡ Electric vehicle batteries

- 🌬️ Wind turbine magnets

- ☀️ Photovoltaic solar panels

- 💧 Hydrogen electrolyzers

- 🛡️ Defense system components

When a single nation controls the supply chain for technologies that define the 21st century economy, every other country faces an uncomfortable reality: their technological future depends on geopolitical relationships that can shift overnight.

China’s Stranglehold on Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026

China’s dominance isn’t accidental—it’s the result of decades of strategic investment while Western nations outsourced production. Today, Chinese companies process approximately 90% of global rare earth oxides, 70% of cobalt, and 60% of lithium[3]. This monopoly extends beyond mining to include the sophisticated processing techniques required to purify these elements to industrial standards.

The Weaponization of Supply Chains

On January 9, 2026, China demonstrated the geopolitical power of this dominance when it began restricting exports of civilian-use rare earths to Japan following comments by Japanese Prime Minister Sanae Takaichi about Taiwan[2]. This wasn’t an isolated incident—it was a calculated demonstration of economic leverage.

The consequences rippled across global industries:

- European automotive firms were forced to halt production and implement layoffs throughout 2025 due to US-China trade restrictions on rare earths

- An Indian electric automotive manufacturer halved its electric scooter output due to rare earths shortages[2]

- Supply chain disruptions cascaded through renewable energy sectors worldwide

“Chinese state-owned companies dominate extraction and processing of critical minerals, giving Beijing control over downstream manufacturing of high-end renewable technologies.”

This structural advantage allows China to influence not just commodity prices, but the pace of technological development in competing nations. When Beijing controls the materials needed for the global transition to renewable energy, it holds tremendous geopolitical leverage.

The Western Response: Building Alternative Supply Chains

Recognizing the strategic vulnerability, Western nations launched an unprecedented coordinated response in 2026. Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026 has triggered the largest peacetime resource mobilization since the Cold War.

United States: Project Vault and Strategic Stockpiling

The Trump administration announced on February 2, 2026, plans to launch a $12 billion critical mineral stockpile—dubbed “Project Vault”—to reduce reliance on China[1]. This represents the most significant government intervention in commodity markets in generations.

Simultaneously, Vice President JD Vance announced a $565 million financing package for Mineração Serra Verde, Brazil’s first rare earth oxides producer, with an option for the US government to take an equity stake[1]. This deal came after Serra Verde strategically cut processing contracts with China to redirect output to Western buyers—a move that signals the beginning of supply chain restructuring.

International Coordination: The Critical Minerals Ministerial

In a high-profile diplomatic push, the Critical Minerals Ministerial convened delegations from 54 countries to coordinate strategy[1][6]. During this gathering, the United States signed 11 new critical-mineral bilateral accords, including:

- A framework with the UAE to accelerate secure supply chains

- A $1 billion joint financing commitment with Australia for critical minerals projects[3][4]

- A 60-day action plan with Mexico to harmonize critical mineral trade policies[1]

This level of coordination demonstrates how seriously Western governments view the threat. The ministerial approach mirrors Cold War-era strategic alliances, adapted for an economic battlefield.

Australia’s Independent Stockpile Strategy

Australia, home to significant rare earth deposits, is establishing an A$1.2 billion strategic stockpile prioritizing antimony, gallium, and rare earth elements[1]. The Australian government is also considering implementing its own price-floor schemes through offtake agreements—a mechanism designed to guarantee minimum prices that make domestic production economically viable even when China floods markets with cheap exports.

Canada’s Emerging Role in Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026

While attention often focuses on US-China rivalry, Canada is quietly positioning itself as a critical supplier to Western allies. The country’s vast mineral wealth, stable governance, and geographic proximity to the United States make it an ideal alternative to Chinese supply chains.

The India Uranium Deal

Canada is nearing a $3 billion uranium deal with India, potentially to be finalized in March 2026[1]. This agreement represents more than just a commercial transaction—it’s part of a broader strategy to integrate democratic nations into secure supply networks that bypass authoritarian control.

Canada’s uranium reserves, combined with its expertise in nuclear technology, position it as a key player in the global energy transition. As nations seek to reduce carbon emissions while maintaining energy security, Canadian uranium becomes increasingly strategic.

North American Integration

The 60-day US-Mexico action plan includes Canada in broader discussions about North American mineral self-sufficiency[1]. This trilateral approach envisions:

- Harmonized mining regulations across borders

- Joint financing for processing facilities

- Coordinated stockpiling strategies

- Border-adjusted price floors for imports

By creating an integrated North American critical minerals ecosystem, these nations aim to replicate China’s vertical integration advantage while maintaining democratic governance and environmental standards. This represents a fundamental shift in how North American nations approach resource development.

The G7 Price Floor Framework: Economic Warfare by Other Means

Perhaps the most innovative response to Chinese dominance is the emerging G7 price floor framework for rare earths, likely to be implemented in 2026[2]. This coordinated mechanism aims to guarantee minimum prices for rare earth elements, fundamentally altering market dynamics.

How Price Floors Work

Traditional commodity markets operate on supply and demand. China has historically used its production capacity to flood markets with cheap rare earths whenever Western competitors emerged, making their projects economically unviable. A coordinated price floor would:

- Guarantee minimum purchase prices for rare earths from approved suppliers

- Protect junior developers whose small projects have uncertain economics

- Encourage investment in Western mining and processing capacity

- Reduce price volatility that has historically deterred development

This approach places growing political pressure on major producers to choose sides—sell to China at market prices, or to the West with price guarantees[2].

Economic Implications

Price floors represent a significant intervention in free markets, but proponents argue national security concerns justify the measure. Critics worry about:

- Potential inefficiencies from artificial pricing

- Retaliation from China through other economic channels

- Compliance challenges across multiple jurisdictions

- Long-term sustainability of government support

Despite these concerns, the framework is moving forward as Western governments conclude that market forces alone cannot overcome China’s structural advantages quickly enough.

The Restructuring of Global Supply Chains

The geopolitical pressure is producing tangible results. Rare earth magnet factories are sprouting up outside China, and previously idled mines in the US and Australia are being reconsidered for reopening as the critical minerals ecosystem is being rewired[1].

Manufacturing Reshoring

Companies that once relied exclusively on Chinese processing are now investing in Western facilities:

| Region | Investment Type | Strategic Importance |

|---|---|---|

| United States | Rare earth processing facilities | Domestic supply security |

| Australia | Magnet manufacturing plants | Indo-Pacific alternative to China |

| Europe | Battery material refineries | EV supply chain independence |

| Canada | Lithium processing | North American integration |

This reshoring doesn’t happen overnight. Building processing facilities requires years of permitting, construction, and operational refinement. The minerals processed in 2026 will power technologies in 2028 and beyond.

Mine Reactivation

Mines shuttered during periods of Chinese price competition are being reassessed. With government backing and price guarantees, projects that were economically marginal become viable. This includes:

- Mountain Pass rare earth mine in California

- Nolans Bore project in Australia

- Various Canadian lithium and rare earth deposits

- Brazilian rare earth developments

Each reactivated mine represents a small reduction in Chinese market share—but collectively, they signal a fundamental shift in global supply chains.

Geopolitical Implications and Future Scenarios

Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026 will shape international relations for decades. Several scenarios could unfold:

Scenario 1: Successful Western Diversification

If current initiatives succeed, by 2030 Western nations could control 30-40% of global processing capacity, significantly reducing Chinese leverage. This would enable:

- More aggressive climate policies without supply chain concerns

- Greater technological independence

- Reduced effectiveness of Chinese economic coercion

Scenario 2: Escalating Economic Warfare

China could respond to Western diversification by:

- Further restricting exports to pressure holdouts

- Undercutting prices to make Western projects uneconomical

- Securing exclusive deals with resource-rich developing nations

- Accelerating development of alternative technologies that don’t require rare earths

Scenario 3: Pragmatic Coexistence

A middle path might emerge where:

- China maintains majority market share but not monopoly control

- Western nations secure enough domestic capacity for critical applications

- Market forces and government intervention find equilibrium

- Both sides avoid escalation that damages global economy

The most likely outcome involves elements of all three scenarios, with periods of tension alternating with pragmatic cooperation as economic and political pressures shift.

Environmental and Ethical Considerations

The race for critical minerals raises important questions about environmental protection and labor standards. China’s dominance partly stems from willingness to accept environmental degradation and lower labor standards that Western nations find unacceptable.

As Western nations expand production, they face pressure to:

- Maintain strict environmental regulations even when they increase costs

- Ensure indigenous rights are respected in mining regions

- Implement responsible waste management for toxic processing byproducts

- Provide fair wages and safe working conditions

These considerations create a competitive disadvantage compared to Chinese operations, but proponents argue they’re essential for sustainable development. The challenge is balancing security imperatives with environmental and social responsibility—a tension that will define resource development in democratic nations.

Conclusion: Navigating the New Reality

Rare Earths and Critical Minerals: The New Battleground for Global Power in 2026 represents a fundamental shift in how nations compete for influence. The elements that power smartphones, electric vehicles, and wind turbines have become as strategically important as oil was in the 20th century.

The Western response—coordinated stockpiling, bilateral agreements, price floors, and supply chain diversification—signals recognition that market forces alone cannot address national security vulnerabilities. China’s willingness to weaponize rare earth exports has accelerated this awakening.

Actionable Next Steps

For policymakers, business leaders, and concerned citizens, several actions can help navigate this new reality:

- Support domestic mining and processing initiatives through investment, policy advocacy, and public education

- Diversify supply chains by sourcing from multiple countries and developing alternative technologies

- Invest in recycling technologies that recover rare earths from electronic waste

- Monitor geopolitical developments that could disrupt supply chains

- Advocate for balanced policies that address security concerns while maintaining environmental standards

The battle for rare earths and critical minerals will define technological leadership, economic prosperity, and military capability for generations. Nations that secure reliable access to these materials will lead the clean energy transition and maintain technological edge. Those that fail risk dependence on geopolitical rivals for the building blocks of modern civilization.

As 2026 progresses, watch for continued announcements of bilateral agreements, stockpile expansions, and mine developments. Each represents another move in the great game for control of the elements that will power the future. The outcome remains uncertain, but the stakes could not be higher.

References

[1] The Critical Minerals Report 02 09 2026 Project Vault And The Wests Scramble For Rare Earths And Price Power – https://investornews.com/critical-minerals-rare-earths/the-critical-minerals-report-02-09-2026-project-vault-and-the-wests-scramble-for-rare-earths-and-price-power/

[2] Ten Global Issues To Shape Mining And Metals Markets In 2026 – https://www.controlrisks.com/our-thinking/insights/ten-global-issues-to-shape-mining-and-metals-markets-in-2026

[3] 010926 Us Eu To Further Intensify Critical Mineral Investments As China Tightens Hold – https://www.spglobal.com/energy/en/news-research/latest-news/metals/010926-us-eu-to-further-intensify-critical-mineral-investments-as-china-tightens-hold

[4] Key Developments In Critical Minerals To Watch In 2026 – https://www.z2data.com/insights/key-developments-in-critical-minerals-to-watch-in-2026

[6] 2026 Critical Minerals Ministerial – https://www.state.gov/releases/office-of-the-spokesperson/2026/02/2026-critical-minerals-ministerial

Some content and illustrations on GEORGIANBAYNEWS.COM are created with the assistance of AI tools.

GEORGIANBAYNEWS.COM shares video content from YouTube creators under fair use principles. We respect creators’ intellectual property and include direct links to their original videos, channels, and social media platforms whenever we feature their content. This practice supports creators by driving traffic to their platforms.

Sharing is SO MUCH APPRECIATED!

{kind=link}