Aging in Place vs. Retirement Communities: The Real Costs in Ontario & Canada 2026

Sharing is SO MUCH APPRECIATED!

When Margaret turned 72, she faced a decision that millions of Canadian seniors confront: should she stay in the Collingwood home where she’d raised her family for 40 years, or move to a retirement community? The answer wasn’t just about comfort or lifestyle—it was about dollars and cents. The debate of aging in place vs. retirement communities has become one of the most critical financial decisions facing Canadian families today, with costs that can vary by tens of thousands of dollars annually.

In 2026, with housing prices remaining elevated across Ontario and Canada, healthcare costs rising, and the senior population growing rapidly, understanding the true financial implications of each option has never been more important. This comprehensive guide breaks down the real costs, hidden fees, and financial considerations to help you or your loved ones make an informed decision.

Key Takeaways

✅ Aging in place in Ontario typically costs between $36,000-$96,000 annually when factoring in home modifications, care services, and maintenance, while retirement communities range from $30,000-$72,000+ per year depending on care level

✅ Hidden costs matter: Both options include unexpected expenses—from emergency response systems and increased home insurance for aging in place, to entrance fees and care level upgrades in retirement communities

✅ Location significantly impacts pricing: Ontario retirement communities in urban centers like Toronto cost 30-50% more than those in regions like Georgian Bay, while property taxes and home maintenance vary widely by municipality

✅ Healthcare needs are the game-changer: As care requirements increase, retirement communities often become more cost-effective due to bundled services, while aging in place can require expensive private care

✅ Quality of life factors have financial implications: Social isolation, safety concerns, and mental health considerations carry both emotional and economic costs that shouldn’t be overlooked

Understanding the True Cost of Aging in Place in Ontario

Aging in place—the ability to live in your own home safely, independently, and comfortably as you grow older—sounds idyllic. For many Canadians, it represents independence, familiarity, and connection to community. But what does it really cost?

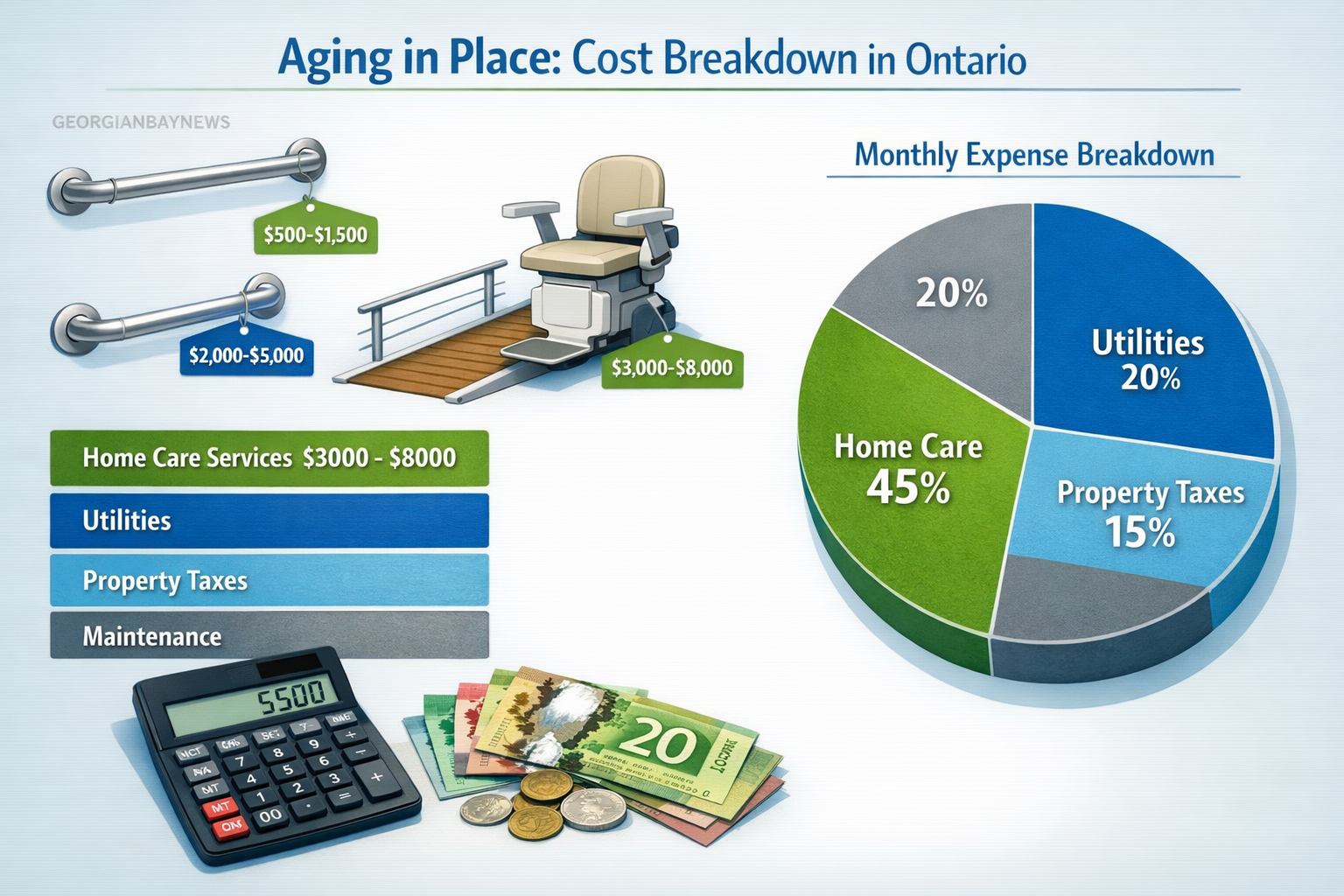

Home Modifications and Accessibility Upgrades

The first major expense category involves making your home safe and accessible. According to the Canada Mortgage and Housing Corporation, the average Canadian spends between $15,000 to $45,000 on home modifications for aging in place[1].

Common modifications include:

- Bathroom renovations with walk-in showers, grab bars, and non-slip flooring: $8,000-$25,000

- Stairlift installation: $3,000-$15,000 depending on stairs

- Wheelchair ramps and widened doorways: $2,000-$8,000

- Kitchen accessibility updates (lowered counters, accessible storage): $5,000-$15,000

- Improved lighting and electrical safety: $1,500-$5,000

John from Thornbury spent $32,000 retrofitting his two-story home in 2025, only to realize two years later that he needed additional modifications as his mobility decreased further. “I wish someone had told me to plan for progressive needs, not just current ones,” he shared.

Ongoing Home Maintenance and Property Costs

Owning a home in Ontario comes with continuous expenses that don’t disappear with age—in fact, they often increase when physical ability to perform DIY maintenance decreases.

Annual costs typically include:

| Expense Category | Annual Cost (Ontario Average) |

|---|---|

| Property taxes | $3,000-$8,000 |

| Home insurance (senior rates) | $1,500-$3,500 |

| Utilities (heating, electricity, water) | $3,600-$6,000 |

| Snow removal and lawn care | $1,200-$3,000 |

| Home repairs and maintenance | $2,000-$5,000 |

| Emergency home repairs | $1,000-$4,000 |

For those living in areas like Georgian Bay, winter maintenance alone can be substantial, with snow removal services becoming essential rather than optional.

Personal Care and Health Services

This is where aging in place costs can escalate dramatically. As health needs increase, so do expenses for professional care services.

Home care costs in Ontario (2026):

- Personal support worker (PSW): $25-$45 per hour

- Registered nurse home visits: $65-$95 per hour

- Occupational therapy: $100-$150 per session

- Meal delivery services: $12-$20 per meal

- Transportation services: $25-$50 per trip

A senior requiring just 4 hours of daily PSW support would spend approximately $36,500-$65,700 annually—and that’s before factoring in nursing care, therapy, or medical equipment[2].

Margaret, whom we met earlier, discovered that her monthly care costs exceeded $5,000 once she needed daily assistance with bathing, medication management, and meal preparation. Combined with her home expenses, she was spending over $90,000 annually to age in place.

Technology and Safety Systems

Modern aging in place relies heavily on technology to ensure safety and maintain independence.

Essential technology costs:

- 📱 Medical alert systems: $30-$60 monthly ($360-$720 annually)

- 🎥 Home monitoring cameras: $200-$800 initial + $10-$30 monthly

- 🏥 Telehealth subscriptions: $50-$150 monthly

- 🔒 Smart home safety devices (automated lighting, fall detection): $500-$2,000 initial investment

These technologies provide peace of mind but represent ongoing expenses that add up over time. For those interested in maintaining wellness at home, resources like stress-relieving exercises and chair yoga for seniors can help maintain physical health affordably.

The Real Costs of Retirement Communities in Ontario

Retirement communities—also called retirement homes or residences—offer a different value proposition: bundled services, social opportunities, and progressive care options all under one roof. But how do the costs compare?

Understanding Retirement Community Fee Structures

Unlike aging in place with its variable costs, retirement communities typically operate on a monthly fee structure that includes multiple services.

Average monthly costs in Ontario (2026):

- Independent living (minimal care): $2,500-$4,500

- Assisted living (moderate care): $3,500-$6,000

- Memory care (specialized dementia care): $5,000-$8,000+

- Full nursing care: $6,000-$10,000+

These fees typically include accommodation, meals, housekeeping, laundry, activities, and basic care services. In regions like Collingwood and The Blue Mountains, prices tend to be 15-25% lower than Toronto or Ottawa[3].

What’s Included vs. What Costs Extra

Understanding what’s bundled versus what requires additional payment is crucial for accurate cost comparison.

Typically included in base fees:

✅ Private or semi-private accommodation

✅ Three meals daily plus snacks

✅ Weekly housekeeping and linen service

✅ Basic utilities (except phone/cable)

✅ 24-hour emergency response

✅ Recreational activities and social programs

✅ Transportation to medical appointments

✅ Basic personal care assistance

Common additional costs:

❌ Entrance or community fees: $1,000-$5,000 (one-time or annual)

❌ Care level increases: $500-$2,000 monthly as needs change

❌ Premium room upgrades: $500-$1,500 monthly

❌ Guest meals: $10-$25 per meal

❌ Beauty salon and spa services: Variable

❌ Premium cable/internet packages: $50-$150 monthly

❌ Pet fees: $25-$100 monthly

Robert moved into a Barrie retirement community in 2024 at the independent living rate of $3,200 monthly. Within 18 months, his care needs increased, bumping his monthly fee to $4,800—a 50% increase he hadn’t fully anticipated.

The Entrance Fee Consideration

Some Ontario retirement communities charge substantial entrance fees (also called “buy-in” fees) ranging from $50,000 to $500,000+. These operate differently:

Two main models:

- Refundable entrance fees: A portion (typically 50-90%) is refunded when you leave or to your estate

- Non-refundable entrance fees: Lower monthly fees but no refund

This model is less common in Ontario than in some U.S. states but exists in premium communities. The financial implications require careful analysis with a financial advisor to determine if the lower monthly fees offset the large upfront investment.

Geographic Cost Variations Across Ontario

Location dramatically impacts retirement community costs within Ontario.

Regional pricing comparison (2026 averages for assisted living):

- Greater Toronto Area: $5,500-$7,500 monthly

- Ottawa: $4,800-$6,500 monthly

- London/Hamilton: $4,000-$5,500 monthly

- Georgian Bay region (Collingwood, Wasaga Beach): $3,800-$5,200 monthly

- Smaller communities (Owen Sound, Orillia): $3,200-$4,800 monthly

For those exploring Ontario adventures or considering different regions, these geographic variations can represent savings of $20,000-$40,000 annually.

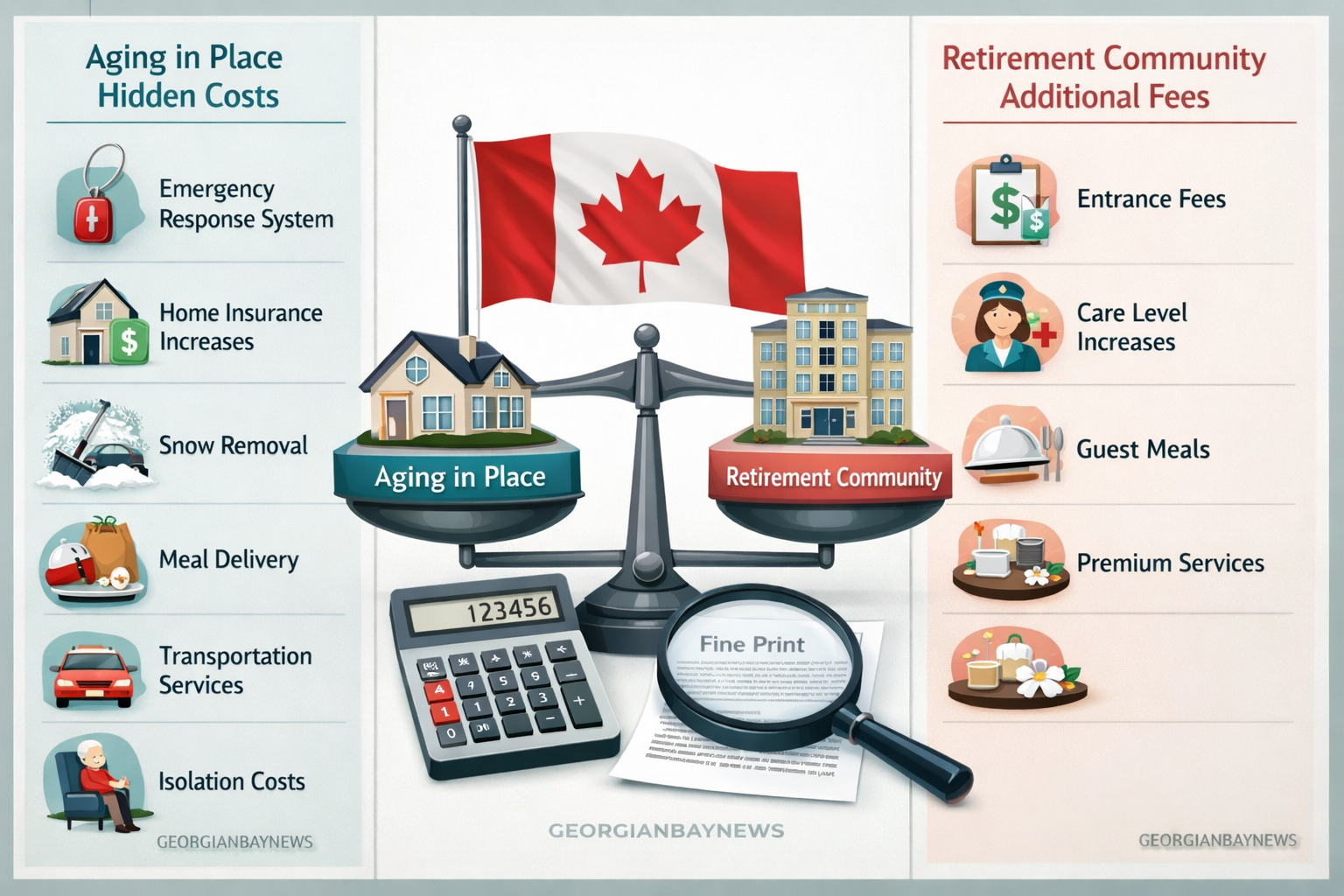

Hidden Costs and Unexpected Expenses: Aging in Place vs. Retirement Communities

Both options come with costs that aren’t immediately obvious but can significantly impact your budget.

Hidden Costs of Aging in Place

Social isolation expenses: Loneliness isn’t just an emotional issue—it has financial implications. Seniors aging in place often spend more on:

- Entertainment and social activities to combat isolation: $100-$300 monthly

- Dining out due to lack of motivation to cook alone: $200-$500 monthly

- Mental health support and counseling: $150-$250 per session

Research shows that social isolation among seniors increases healthcare costs by an average of $6,700 annually due to depression, cognitive decline, and physical health deterioration[4].

Emergency and crisis costs: When living alone, emergencies can be more expensive:

- Emergency room visits due to falls or delayed care: $500-$2,000 per incident

- Temporary rehabilitation or respite care: $200-$400 daily

- Emergency home repairs (burst pipes, heating failures): $1,000-$10,000

Family caregiver costs: Often overlooked, family members providing care face their own financial impacts:

- Lost wages from reduced work hours: Variable, potentially $10,000-$50,000 annually

- Travel expenses for distant family members: $200-$500 monthly

- Stress-related health impacts on caregivers: Difficult to quantify but significant

For family caregivers seeking support, resources on stress management and self-regulation techniques can be invaluable.

Hidden Costs of Retirement Communities

Care level creep: As mentioned earlier, most residents experience care level increases over time. What starts as independent living often progresses to assisted living, then potentially memory or nursing care—each with substantial fee increases.

Social pressure spending: Living in a community environment can create subtle financial pressures:

- Participating in optional activities with fees: $50-$200 monthly

- Contributing to group gifts and social events: $30-$100 monthly

- Keeping up with community standards (clothing, personal care): Variable

Healthcare gaps: Retirement communities aren’t hospitals. Additional healthcare costs may include:

- Specialized medical equipment not provided: $500-$5,000

- Prescription medications: $100-$500 monthly

- Specialist medical appointments and treatments: Variable

- Dental, vision, and hearing care: $1,000-$5,000 annually

Transition costs: Moving to a retirement community involves one-time expenses:

- Downsizing and estate sales: $500-$3,000 in fees

- Moving services: $1,000-$5,000

- Selling your home (if applicable): Realtor fees, legal costs, potential capital gains tax

- Furnishing and setting up new accommodation: $2,000-$10,000

Making the Financial Decision: Which Option Makes Sense for You?

The aging in place vs. retirement communities debate isn’t one-size-fits-all. The right financial choice depends on multiple personal factors.

When Aging in Place Makes Financial Sense

Aging in place may be more cost-effective when:

✅ Your home is already accessible or requires minimal modifications

✅ You’re in good health with minimal care needs currently and in the foreseeable future

✅ Your home is paid off or has a very low mortgage

✅ You have strong family or community support reducing paid care needs

✅ You live in a lower-cost region with affordable home maintenance services

✅ You have long-term care insurance covering home care services

Financial profile example:

Sarah, 68, owns her accessible bungalow in Owen Sound outright. She’s in excellent health, has a strong social network, and her daughter lives nearby. Her annual costs:

- Property taxes and insurance: $4,200

- Utilities and maintenance: $6,500

- Occasional home care (10 hours monthly): $3,600

- Total: $14,300 annually

For Sarah, aging in place is significantly more affordable than a retirement community at $42,000-$60,000 annually.

When Retirement Communities Make Financial Sense

Retirement communities often become more cost-effective when:

✅ Care needs are moderate to high requiring daily assistance

✅ Social isolation is a concern and you value community engagement

✅ Home maintenance is burdensome physically or financially

✅ Safety is a priority and you live alone

✅ You want predictable monthly expenses rather than variable costs

✅ Your home requires significant accessibility modifications

Financial profile example:

David, 76, lives alone in a two-story Toronto home. He has mobility challenges, diabetes requiring daily management, and needs help with bathing and meal preparation. His annual aging in place costs:

- Property taxes and insurance: $7,500

- Utilities and maintenance: $8,000

- Daily PSW care (4 hours): $52,000

- Meal delivery: $6,000

- Medical alert and technology: $1,500

- Total: $75,000 annually

For David, an assisted living retirement community at $60,000-$72,000 annually offers similar or better value with added safety, social opportunities, and comprehensive services.

The Break-Even Analysis

Financial advisors recommend conducting a break-even analysis comparing both options over 5-10 years, factoring in:

- Current costs for each option

- Projected care need increases (most seniors require more care over time)

- Inflation rates for healthcare (typically 3-5% annually) and housing costs

- Potential home sale proceeds if moving to a retirement community

- Investment returns if proceeds are invested rather than tied up in home equity

- Quality of life value (harder to quantify but important)

Many families discover that while aging in place may be cheaper initially, the financial equation shifts as care needs increase. Planning for this transition point is crucial.

Government Support and Financial Assistance

Both options may qualify for various forms of financial support in Ontario and Canada:

For aging in place:

- Home Accessibility Tax Credit (federal): Up to $10,000 in eligible expenses

- Ontario Seniors’ Home Safety Tax Credit: Up to $2,500 in eligible expenses

- Veterans Independence Program: Home care and maintenance for eligible veterans

- Ontario Health Home Care: Subsidized home care services (eligibility-based)

For retirement communities:

- Medical expense tax deductions: Eligible care costs may be claimed

- Provincial subsidies: Limited subsidized beds available (long waiting lists)

- Veterans benefits: May cover portions of retirement community costs

- Long-term care insurance: If purchased earlier, may cover retirement community fees

Understanding these programs can reduce out-of-pocket costs significantly. Consulting with a financial planner familiar with senior benefits is highly recommended.

For those managing budgets carefully, exploring frugal living tips can help stretch retirement dollars further.

Beyond the Numbers: Quality of Life Considerations

While this article focuses on financial costs, the aging in place vs. retirement communities decision involves factors that transcend dollars and cents.

Social Connection and Mental Health

Research consistently shows that social connection is one of the strongest predictors of healthy aging. Retirement communities offer built-in social opportunities—daily activities, communal dining, hobby groups, and friendships with peers.

Conversely, aging in place in familiar surroundings provides connection to long-established community ties, neighbors, and local organizations. For some, this is irreplaceable; for others, these connections naturally diminish over time as friends move or pass away.

The mental health implications of isolation or community engagement have real healthcare costs. Depression and cognitive decline accelerate when seniors are isolated, potentially increasing medical expenses by thousands annually[5].

Resources like Buddhist principles for emotional resilience and understanding what people regret most can provide perspective on these important life decisions.

Safety and Peace of Mind

Falls are the leading cause of injury among Canadian seniors, with one in three adults over 65 experiencing a fall annually[6]. The financial cost of fall-related injuries averages $20,000-$40,000 when factoring in medical care, rehabilitation, and potential long-term care needs.

Retirement communities offer 24/7 staff presence, emergency call systems in every room, and immediate response capabilities. For aging in place, safety depends on technology, personal vigilance, and hope that help arrives quickly when needed.

The “peace of mind” factor—for both seniors and their families—has intangible value that some families consider priceless, while others manage successfully with technology and planning.

Independence and Control

For many Canadians, independence is paramount. Aging in place offers maximum control over daily routines, meal choices, visitors, pets, and lifestyle. Your home, your rules.

Retirement communities, while offering many choices, operate within community guidelines—meal times, visiting hours, pet policies, and community standards. For some, this structure is welcome; for others, it feels restrictive.

The question becomes: is the independence of aging in place worth the potential financial premium and safety risks? Or does the supported independence of a retirement community—freedom from maintenance worries with professional care available—offer a better quality of life?

Family Impact

The decision affects entire families. Adult children often become primary caregivers, coordinators of care, or emergency contacts. The emotional and financial burden on families supporting aging in place can be substantial.

Retirement communities can reduce family caregiver burden significantly, allowing adult children to focus on quality time with parents rather than care coordination and crisis management. However, some families deeply value the opportunity to care for aging parents at home, seeing it as an honor and responsibility.

Conclusion: Making Your Decision

The aging in place vs. retirement communities financial comparison reveals that there’s no universally “cheaper” option—it depends entirely on individual circumstances, health status, location, and care needs.

Key decision-making steps:

- Assess current and projected care needs honestly: Consult with healthcare providers about realistic care trajectories

- Calculate comprehensive costs for both options: Include all categories discussed in this article, not just obvious expenses

- Factor in geographic variations: Consider whether relocating to a lower-cost region makes sense

- Evaluate home equity: If your home has significant equity, analyze whether that capital could be better deployed

- Consider quality of life factors: Assign value to social connection, safety, and independence based on personal priorities

- Plan for transitions: Recognize that today’s choice may not be permanent; plan for flexibility

- Consult professionals: Work with financial planners, elder care advisors, and healthcare providers for personalized guidance

- Visit multiple retirement communities: If considering this option, tour facilities, talk to residents, and understand exactly what you’re getting

- Trial periods: Some communities offer short-term stays; some seniors try aging in place with increasing supports before making permanent decisions

- Review regularly: Circumstances change; revisit the decision annually or when health status shifts

Action steps for readers:

📋 Create a comprehensive cost spreadsheet comparing both options with your specific numbers

🏥 Schedule a healthcare assessment to understand current and future care needs

💰 Consult a financial advisor familiar with senior living options and benefits

🏘️ Research local retirement communities and request detailed fee schedules

🏠 Get home accessibility assessments to understand modification costs if aging in place

👨👩👧👦 Have family discussions about expectations, support availability, and preferences

The decision between aging in place and retirement communities is deeply personal, with financial implications that can span decades and hundreds of thousands of dollars. By understanding the real costs—both obvious and hidden—Canadian seniors and their families can make informed choices that support both financial security and quality of life in the years ahead.

Remember, this isn’t a one-time decision. Many seniors successfully age in place for years before transitioning to retirement communities when care needs increase. Others move to retirement communities early and thrive in the social environment. The key is making an informed choice based on accurate financial information, realistic health projections, and personal values.

For more information and community resources, visit Georgian Bay News for local updates and senior-focused content.

References

[1] Canada Mortgage and Housing Corporation. (2025). “Home Adaptations for Seniors: Cost Analysis and Guidelines.” CMHC Research Reports.

[2] Ontario Personal Support Workers Association. (2026). “2026 Home Care Cost Survey: Ontario Rates and Trends.”

[3] Ontario Retirement Communities Association. (2026). “Annual Fee Structure Report: Regional Cost Variations Across Ontario.”

[4] National Institute on Ageing, Toronto Metropolitan University. (2024). “Social Isolation and Healthcare Costs Among Canadian Seniors.”

[5] Canadian Mental Health Association. (2025). “Mental Health and Aging: The Financial Impact of Isolation and Depression.”

[6] Public Health Agency of Canada. (2025). “Falls Among Canadian Seniors: Incidence, Costs, and Prevention Strategies.”

Some content and illustrations on GEORGIANBAYNEWS.COM are created with the assistance of AI tools.

Sharing is SO MUCH APPRECIATED!

{kind=link}