Global Fertilizer Shortages in the World: A Deep Analysis (2026)

Last updated: May 23, 2026

Quick Answer: Fertilizer shortages in the world are driven by a combination of geopolitical conflict, energy price spikes, trade restrictions, and supply chain disruptions. These shortages are pushing food production costs higher across every continent, threatening food security for hundreds of millions of people — particularly in lower-income nations. Canada and the USA are not immune, facing significant price volatility and input cost pressures on their farming sectors.

Key Takeaways

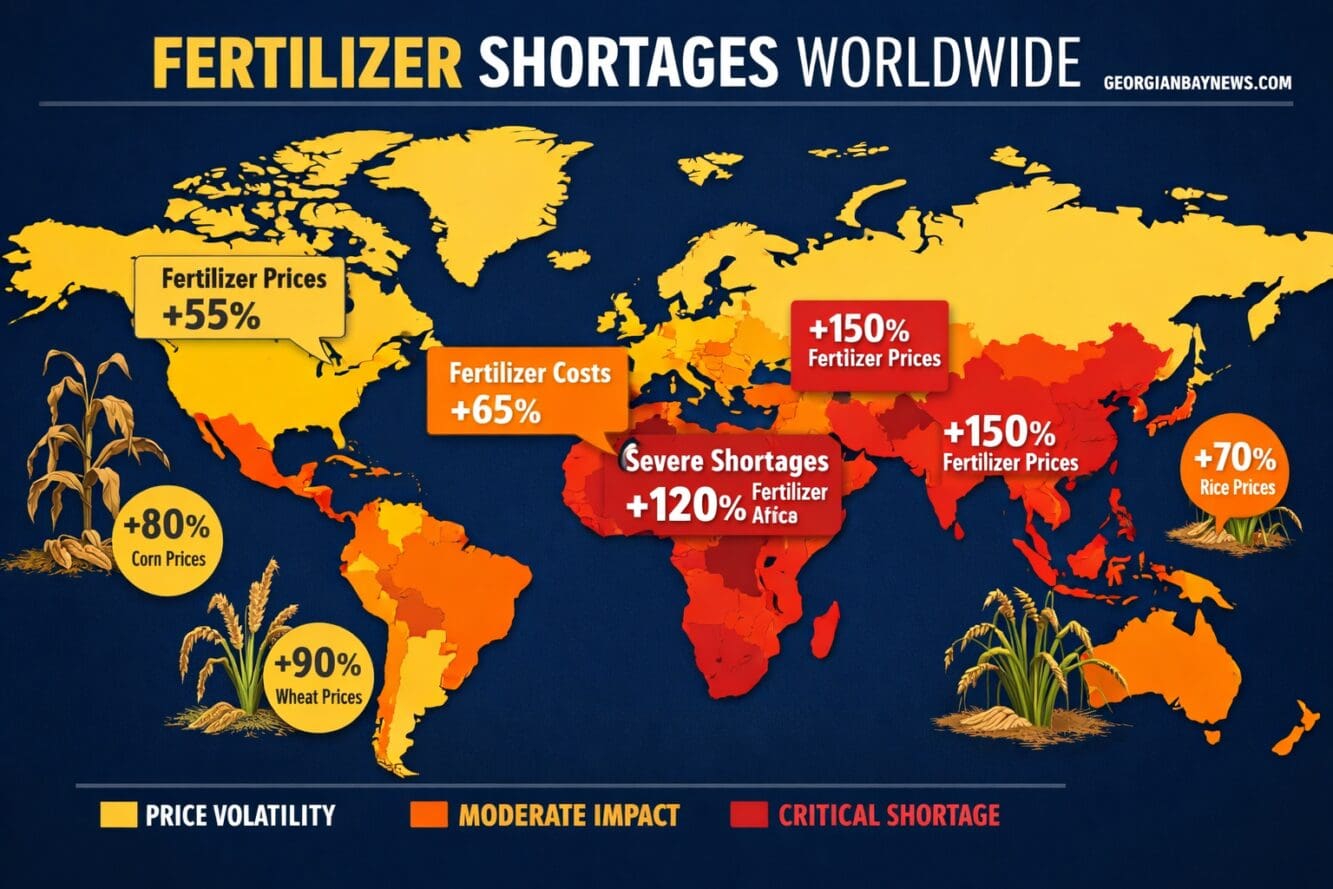

- Russia and Belarus together supply roughly 40% of the world’s potash, making the war in Ukraine and related sanctions a direct driver of global fertilizer supply disruptions (World Bank, 2022).

- Nitrogen fertilizer prices surged more than 200% between 2020 and 2022, with prices remaining elevated well above pre-pandemic levels through 2025–2026 (FAO, 2022).

- Sub-Saharan Africa and South Asia are the most severely impacted regions, where smallholder farmers have little ability to absorb price shocks.

- Canada is one of the world’s largest potash producers, yet domestic farmers still face cost pressures due to global price benchmarking and natural gas-linked nitrogen costs.

- American farmers have reduced fertilizer application rates in response to price spikes, with potential long-term yield consequences for corn and wheat.

- Organic farming, precision agriculture, and biofertilizers offer partial but not complete substitutes for synthetic fertilizers at current scale.

- Long-term solutions include diversifying supply chains, investing in green ammonia production, and expanding domestic fertilizer manufacturing capacity.

What Is Causing Global Fertilizer Shortages Right Now?

Fertilizer shortages in the world stem from several overlapping crises hitting simultaneously. The three main fertilizer types — nitrogen, phosphorus, and potassium (NPK) — each face distinct supply pressures.

- Nitrogen fertilizers are manufactured from natural gas. When European energy prices spiked after 2021, many nitrogen plants reduced or halted production, cutting global supply.

- Potash supply was severely disrupted when Western nations sanctioned Belarus and Russia following the 2022 invasion of Ukraine. Together, these two countries account for a large share of global potash exports.

- Phosphate supply has been affected by export restrictions from China and Morocco’s dominance of global reserves.

Add to this: pandemic-era shipping bottlenecks, port congestion, and a general retreat from global trade integration — and the result is a market where supply cannot keep pace with agricultural demand.

What Role Do Russia and Ukraine Play in Global Fertilizer Markets?

Russia and Ukraine are central to the global fertilizer crisis. Russia is the world’s largest exporter of nitrogen fertilizers and a top-three exporter of both potash and phosphate, according to the Food and Agriculture Organization (FAO, 2022). Ukraine, while not a major fertilizer producer, is a critical grain exporter whose reduced output increases pressure on farmers worldwide to maximize yields — which requires more fertilizer, not less.

When sanctions were applied to Russia and Belarus following the 2022 invasion, global potash supply dropped sharply. Countries that relied heavily on Russian ammonia pipelines through Ukraine lost access almost overnight. The ripple effect reached grain farmers in Iowa, canola growers in Saskatchewan, and rice farmers in Bangladesh alike.

“The war in Ukraine didn’t just disrupt grain markets — it struck at the very inputs farmers need to grow food in the first place.” — FAO, 2022

How Are Fertilizer Shortages Affecting Food Production Worldwide?

Reduced fertilizer availability directly lowers crop yields. Nitrogen is essential for plant growth; without adequate application, staple crops like corn, wheat, and rice produce significantly less per acre.

Key impacts on food production include:

- Lower yields per hectare for nitrogen-dependent crops, particularly corn and wheat

- Higher food prices passed from farmers to consumers globally

- Reduced planted acreage in some regions where input costs make farming unprofitable

- Soil degradation in areas where farmers skip fertilizer applications entirely over multiple seasons

In the USA, the USDA reported that corn growers reduced nitrogen application rates in 2022–2023 in response to cost pressures, with yield impacts varying by region. In Canada, Prairie grain farmers faced input cost increases that squeezed margins even as commodity prices rose. You can explore more about government spending and agricultural subsidies and how policy shapes farming economics.

Which Countries Are Most Impacted by Current Fertilizer Supply Issues?

Developing nations bear the heaviest burden, but no region is untouched. Countries most severely affected include:

RegionKey IssuePrimary Crops at RiskSub-Saharan AfricaCannot afford price spikes; low subsidy capacityMaize, sorghum, cassavaSouth AsiaHeavy dependence on imported ureaRice, wheatLatin AmericaReliance on Russian potash exportsSoybeans, coffee, sugarEuropeEnergy-linked nitrogen production cutsWheat, barleyUSAPrice volatility; corn belt input costsCorn, soybeansCanadaPotash producer but price-exposedCanola, wheat, barley

Canada is in a unique position: it holds some of the world’s largest potash reserves, primarily in Saskatchewan. Yet Canadian farmers still pay globally benchmarked prices for nitrogen fertilizers, which are tied to natural gas costs. The solutions being explored at the policy level include strategic reserves and domestic production incentives.

How Much Have Fertilizer Prices Increased?

Fertilizer prices rose dramatically between 2020 and 2022 and remain elevated. According to the World Bank Commodity Price Data (2022), urea prices increased by over 200% from pre-pandemic levels at their peak. Diammonium phosphate (DAP) and potash (MOP) saw similar surges.

By 2024–2025, prices moderated somewhat from peak levels but remained 50–80% above 2019 baselines, according to FAO commodity tracking. For North American farmers, this translated directly into higher per-acre input costs — in some cases adding $150–$200 per acre to corn production expenses (estimates based on USDA input cost surveys, 2023).

Will Fertilizer Shortages Lead to Food Insecurity?

Yes, and in some regions, food insecurity is already a direct consequence. The UN World Food Programme warned in 2022 that reduced fertilizer use could lead to a global food production shortfall affecting hundreds of millions of people.

The risk is highest where:

- Smallholder farmers have no access to credit or subsidies

- Governments lack foreign exchange to import fertilizers

- Alternative soil amendments are not available or affordable

In wealthier nations like the USA and Canada, food insecurity from fertilizer shortages is indirect — felt through higher grocery prices rather than outright crop failure. But for countries in East Africa or South Asia, the link between fertilizer access and caloric sufficiency is direct and urgent. Understanding states of emergency declared in food-stressed regions helps illustrate just how acute this crisis has become.

How Are Developing Countries Dealing With Fertilizer Supply Problems?

Developing nations are responding with a mix of emergency subsidies, import diversification, and promotion of alternative inputs. Several approaches are being used:

- Government subsidies to buffer retail fertilizer prices for smallholders (used in India, Kenya, and Ethiopia)

- Barter and bilateral trade deals to secure supply outside Western-sanctioned channels

- Promotion of organic amendments such as compost, manure, and biochar

- Emergency food aid coordination through the World Food Programme

However, subsidies are fiscally unsustainable for many low-income governments, and alternative inputs cannot fully replace synthetic fertilizers at scale in the short term.

What Alternatives Do Farmers Have When Fertilizer Is Scarce?

When synthetic fertilizers are unavailable or unaffordable, farmers have several options — each with trade-offs.

Short-term alternatives:

- Compost and animal manure (widely available but lower nutrient density)

- Crop rotation with nitrogen-fixing legumes (e.g., soybeans, clover)

- Reduced-rate application with precision placement technology

Emerging alternatives:

- Biofertilizers using nitrogen-fixing bacteria (e.g., Rhizobium inoculants)

- Slow-release fertilizers that improve efficiency and reduce total volume needed

- Foliar feeding for micronutrient supplementation

The honest limitation: none of these fully replaces synthetic NPK for high-yield commodity crops at current scales. They work best as complements, not replacements.

Can Organic Farming Help Reduce Fertilizer Dependency?

Organic farming methods can meaningfully reduce reliance on synthetic fertilizers, but they cannot solve the global shortage alone. Organic systems typically yield 20–25% less than conventional systems for staple crops, according to a meta-analysis published in Nature (Seufert et al., 2012) — a gap that matters enormously when feeding a global population of 8+ billion.

That said, organic and regenerative practices offer real benefits:

- Build long-term soil health, reducing future fertilizer needs

- Lower input costs for farmers willing to accept yield trade-offs

- Reduce environmental runoff from excess nitrogen and phosphorus

For Canadian and American farmers, integrating cover crops and reduced-tillage practices alongside targeted synthetic fertilizer use is the most practical near-term path. Exploring solar energy and other sustainable inputs can also support the broader shift toward lower-emission agriculture.

What Are the Environmental Consequences of Reduced Fertilizer Use?

Reduced fertilizer use has a paradox: it can be both environmentally beneficial and harmful, depending on the context.

Potential benefits:

- Less nitrogen runoff into waterways, reducing algal blooms and dead zones

- Lower nitrous oxide (N₂O) emissions, a potent greenhouse gas

- Reduced groundwater contamination

Potential harms:

- Farmers expanding into marginal or forested land to compensate for lower yields

- Soil nutrient depletion over multiple seasons without replacement

- Increased pressure on natural ecosystems to meet food demand

The net environmental outcome depends heavily on how farmers adapt — and whether policy supports sustainable intensification rather than land expansion.

How Are Agricultural Tech Companies Responding to Fertilizer Supply Issues?

Agricultural technology companies are accelerating development of precision tools and biological alternatives. Key responses include:

- Precision application technology (variable-rate spreaders, drone application) that reduces total fertilizer use by 15–30% without yield loss

- Soil sensing platforms that give real-time nutrient data, preventing over-application

- Synthetic biology startups engineering nitrogen-fixing microbes for non-legume crops

- Green ammonia projects using renewable electricity to produce nitrogen fertilizer without natural gas

In Canada and the USA, companies and universities (including research partnerships noted at Stanford University) are investing in next-generation soil health technologies. The spending commitments from both public and private sectors are growing, though commercial scale remains years away for most biological alternatives.

What Long-Term Solutions Are Being Developed to Address Fertilizer Supply Challenges?

Long-term solutions to fertilizer shortages in the world require action at multiple levels simultaneously.

Policy-level solutions:

- Diversifying import sources and building strategic fertilizer reserves

- Reducing trade restrictions on fertilizer exports during crisis periods

- Expanding domestic production capacity in import-dependent nations

Technology-level solutions:

- Green ammonia (hydrogen-based nitrogen production using renewable energy)

- Enhanced efficiency fertilizers (EEFs) that reduce application volumes

- Bioengineered crops with improved nutrient uptake efficiency

Farm-level solutions:

- Soil health programs that reduce long-term fertilizer dependency

- Integrated nutrient management combining organic and synthetic inputs

The stakeholders involved — governments, agribusinesses, NGOs, and farmers — must coordinate across these levels for any solution to be durable. No single fix will resolve a problem this structurally complex.

Conclusion: What Should Farmers, Policymakers, and Consumers Do Now?

Fertilizer shortages in the world are not a temporary blip — they reflect deep structural vulnerabilities in global food systems. The convergence of geopolitical conflict, energy price volatility, and supply chain fragility has exposed how dependent modern agriculture is on a handful of input sources.

Actionable next steps by audience:

- Farmers (Canada & USA): Audit soil health now, invest in precision application technology, and explore cover crop rotations to reduce long-term fertilizer dependency.

- Policymakers: Prioritize strategic fertilizer reserves, incentivize domestic production, and reduce export restrictions during supply crises.

- Consumers: Support food policy advocacy and understand that food price increases are partly a fertilizer story — pressure on input costs flows directly to grocery shelves.

- Investors and agribusinesses: Monitor green ammonia development and precision agriculture platforms as both risk-mitigation and growth opportunities.

The global food system can adapt — but only if the urgency of fertilizer supply security receives the same attention as energy security. The time to act is before the next shortage, not during it.

FAQ

Q: What are the three main types of fertilizer affected by shortages?

Nitrogen (N), phosphorus (P), and potassium (K) — the NPK trio — are all affected, though nitrogen and potash face the most acute supply disruptions as of 2026.

Q: Is Canada a fertilizer producer or importer?

Canada is both. It is one of the world’s largest potash exporters (primarily from Saskatchewan), but it imports significant quantities of nitrogen and phosphate fertilizers, making it partially exposed to global price swings.

Q: Why does natural gas affect fertilizer prices?

Natural gas is the primary feedstock for producing ammonia, the base of most nitrogen fertilizers. When gas prices rise, nitrogen fertilizer production costs rise in direct proportion.

Q: Which fertilizer type is most critical for corn production?

Nitrogen is the most critical input for corn. Corn is one of the most nitrogen-intensive crops, and reduced nitrogen application has a direct and measurable impact on yield per acre.

Q: Are fertilizer prices in 2026 still elevated?

Yes. While prices have declined from their 2022 peak, they remain significantly above 2019 pre-pandemic baselines, according to FAO commodity tracking data through 2025.

Q: What is green ammonia?

Green ammonia is nitrogen fertilizer produced using hydrogen generated from renewable electricity (electrolysis) rather than natural gas. It offers a low-carbon alternative but remains more expensive than conventional ammonia at current scale.

Q: How do fertilizer shortages affect food prices for consumers?

Higher fertilizer costs increase farmers’ input expenses, which are partially passed on through the supply chain. Staple foods like bread, corn products, and cooking oils are most directly affected.

Q: Can biofertilizers fully replace synthetic fertilizers?

Not yet at commercial scale. Biofertilizers work well as supplements and can reduce synthetic fertilizer needs by 20–30% in some systems, but they cannot fully replace NPK inputs for high-yield commodity crop production.

Q: What did the Russia-Ukraine war do to potash supply?

Sanctions on Russia and Belarus — which together supply an estimated 40% of global potash — removed a major portion of world supply from accessible markets, causing prices to spike sharply in 2022 (World Bank, 2022).

Q: What can individual farmers do right now?

Soil test before every planting season, use precision application equipment to avoid waste, integrate legume cover crops, and explore slow-release or enhanced efficiency fertilizer products to stretch available supply further.

References

- Food and Agriculture Organization of the United Nations (FAO). Fertilizer Outlook and Policy Brief. 2022. https://www.fao.org

- World Bank. Commodity Markets Outlook: Fertilizer Price Surge. 2022. https://www.worldbank.org

- Seufert, V., Ramankutty, N., & Foley, J.A. Comparing the yields of organic and conventional agriculture. Nature, 485, 229–232. 2012. https://www.nature.com/articles/nature11069

- USDA Economic Research Service. Fertilizer Use and Price. 2023. https://www.ers.usda.gov

- UN World Food Programme. Global Food Crisis Report. 2022. https://www.wfp.org

Content, illustrations, and third-party video appearing on GEORGIANBAYNEWS.COM may be generated or curated with AI assistance or reproduced pursuant to the fair dealing provisions of the Copyright Act, R.S.C. 1985, c. C-42. Attribution and hyperlinks to original sources are provided in acknowledgment of applicable intellectual property rights. Such referencing is intended to direct traffic to and support the original rights holders’ platforms.

{kind=link}